Navegación

Cerrar

Servicios

Gestión Patrimonial

Su patrimonio no es solo cuestión de números. Su patrimonio cuenta su historia, sus valores, sus ilusiones y visión de futuro. Nuestra misión es dedicar tiempo para escuchar y entender esa visión, y así después crear estrategias para sus activos que se puedan materializar.

Planificación patrimonial

Como empresa familiar con más de 200 años de historia, tenemos un profundo conocimiento de lo que significa el espíritu emprendedor. A lo largo de los años, lo hemos visto todo: incertidumbres, éxitos, retos, subidas y bajadas. En resumen, sabemos por lo que usted está atravesando al construir y desarrollar su negocio y queremos ayudarle a tener éxito.

Los emprendedores son la fuerza que impulsa nuestra economía. Asumen riesgos, innovan y crean riqueza para ellos mismos y para la sociedad en general. Nuestro objetivo es ser un socio de confianza para los emprendedores, ya sea que estén empezando o pasando al siguiente nivel. Estamos preparados para ayudarle en cualquier momento del recorrido de su negocio.

Contacte con nosotros

Wealth management

Managing director

Wealth management

Head of Wealth Management France

Corporate finance

Head of Corporate Finance & Capital Markets

Corporate finance

Head of Mirabaud Advisors, France

Contáctenos

Paris

Madrid

Paris

Paris

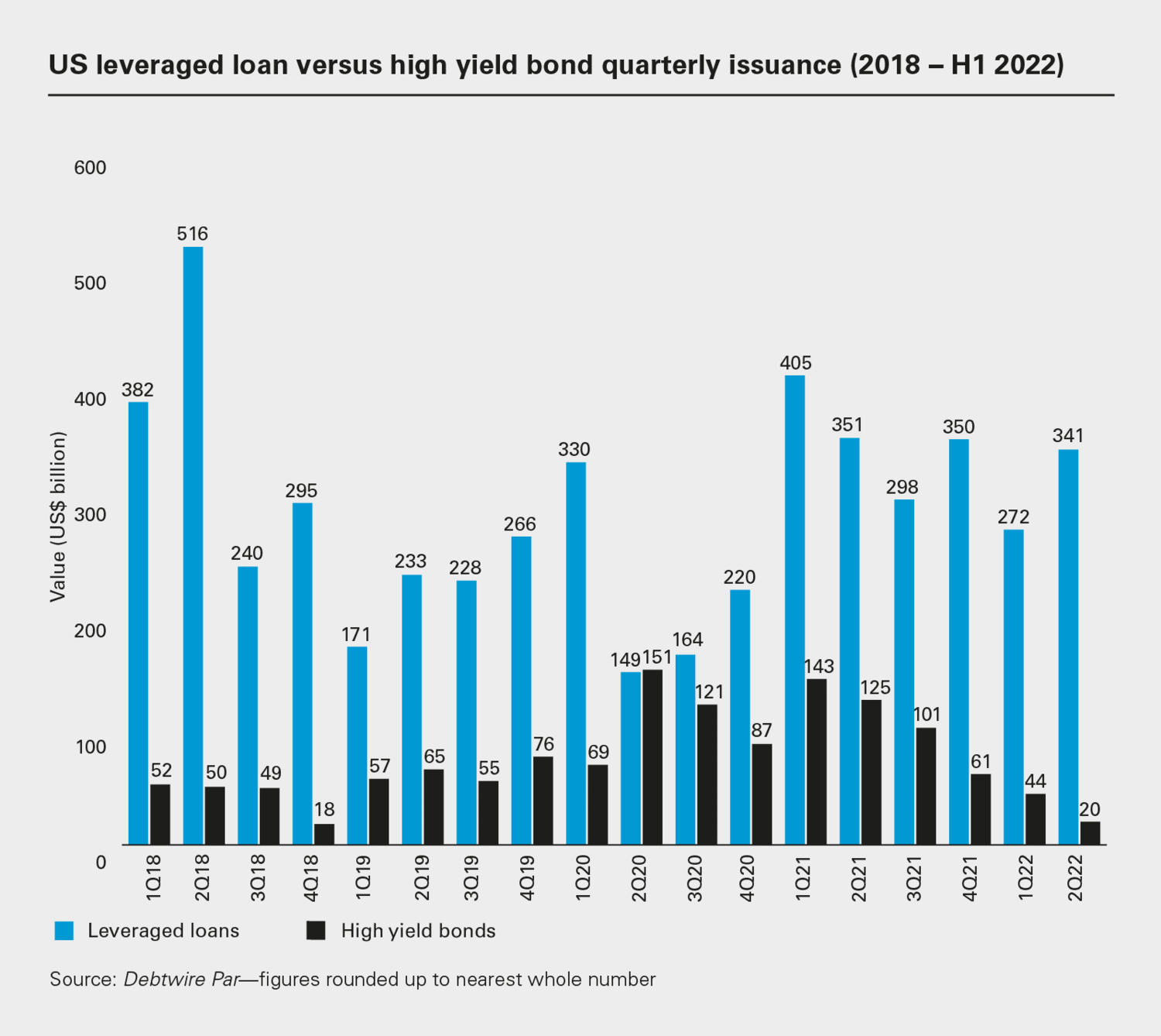

The shift toward growth and economic dynamism in a scenario of extremely low rates and excess liquidity only worsened the overindebtedness of national and private accounts and contributed to the creation of the perception of an absence of credit risk. For debt-securities markets, especially insofar as national debt, this meant lower interest rates and the narrowing of the bond yield spreads of peripheral economies, due to quantitative flexibilisation and tightening credit spreads. The result is that investors seeking return in a context of negative rates are forced to turn to alternative strategies that they would not consider otherwise. Some of them invest in companies with lower creditworthiness or less liquid assets as a means of obtaining higher rates of return than that of interest rates. This extremely pernicious scenario led to global rate markets seeing all-time-low rates across the curve and a strong liquidity-driven rally across equity, debt, commodity and new-age investments.

And suddenly (or very quickly, in any case), as a result of such an unprecedented and unforeseeable event, the pandemic further complicated the macroeconomic scenario, taking a toll on the worldwide economy the likes of which we have not seen since the Great Depression, and forcing central banks to take decisive action to regain economic growth. The Federal Open Market Committee lowered its target rate by 50bps to 1%–1.25% in March 2020 and announced plans to increase its holdings in Treasuries and mortgage-backed securities by at least USD500bn and USD200bn, respectively. The European Central Bank, while keeping its refinancing rate unchanged at 0%, introduced its staggered stimulus measures, with peak asset purchases of EUR1,850bn. The Bank of England (BoE) cut its base rate to 0.25% in March 2020 from 0.75% and then to 0.10%. For two decades, we had benefitted from considerable stability of worldwide growth and inflation, but all of that came to an end, and we found ourselves in a demand-driven economy with readily available supply that was abruptly cut off.

Bottlenecks and Russia’s invasion of Ukraine have given rise to geopolitical tensions and supply-side shortages, causing delays in supply chains and higher commodities prices, especially gas, and Europe is now seriously eyeing a potential lack of supply. Among other consequences, this has brought on surging inflation worldwide and extremely restrictive and accelerated monetary policy in response. The Fed has implemented the fastest rates increase since 1980.

Now is the time for central banks and investors to consider and evaluate the immediate impact of these restrictive policies as well as their consequences in the long term.

It is clear that the fundamentals of the US and European economies have weakened in 2022, as reduced fiscal benevolence, tightening monetary policy and rising prices have weighed on consumption. The fact is that these negative trends gathered over the course of 2021 are not new to investors. What has shifted more rapidly is how they interpret these fundamentals, creating a context of tumultuous volatility that we have not seen in years.

Negative macroeconomic trends, persistent global inflation, tightening monetary policy, a surging US dollar and global slowing of consumption may well drive us into recession. But should investors fear a severe worldwide credit crisis or focus their concern on the repricing of credit markets?

There are a number of facts that lead to the belief that we should, at least, go much wider than actual levels:

We are amid a relief rally brought on by the continued solidity of 3Q corporate earnings, some easing of inflation and a slightly less hawkish tone from the Fed. These factors have allowed credit indices to regain much of the ground lost year to date and are putting a squeeze on supply that is accelerating market recovery. This tone is striking as being highly complacent, considering the abundance of flagged alerts. From this point onward, the main driver for markets will likely be, once again, actions taken by central banks.

As Sgt. Esterhaus used to say on Hill Street Blues in the mid-1980s, “Let’s be careful out there”.

Por favor no dude en comunicarse con su persona de confianza en Mirabaud o contáctenos aquí si este tema es de su interés. Junto a nuestros dedicados especialistas estaremos encantados de evaluar sus necesidades personales y discutir posibles soluciones de inversión adaptadas a su situación.

Continuar con

Asset Management