The hegemony of the dollar has recently come into question, as US competitiveness is at the front of the Trump administration policies. The trade war, the attacks on the independence of the Federal Reserve and its Chair, Jerome Powell, and fears of US sovereign debt restructuring has dented confidence in the dollar.

Foundations of the dollar dominance

For most of the last century, the international role of the dollar has been supported by the size and strength of the US economy, deep and liquid capital markets and a smooth functioning of the financial system. This role can be explained from two different perspectives:

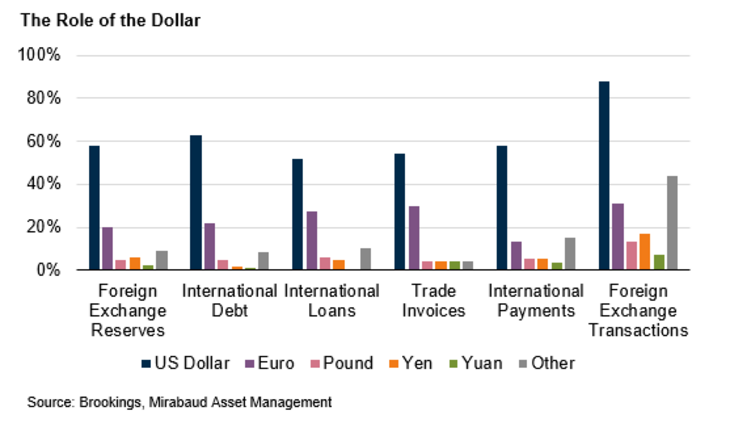

1. The trade view: The dominance of the US dollar in trade invoicing is a key reason for its significant role in the global economy. The dollar's share in trade invoicing is much larger than the US share of global exports and imports of traded goods. There is a fundamental connection between the dollar’s role as the currency in which non-US exporters predominantly invoice their sales, and its prominence in global banking and finance. This widespread use of the dollar in international trade increases the demand for safe dollar deposits and lowers borrowing costs.

2. The safe asset view: There is a high global demand for safe assets, and US government debt is considered one of the safest places to invest. The dollar makes up more than 50% of the world's official foreign exchange reserves, acting as a reliable store of value.

Current threats to the dollar

However, investors are now questioning whether the US is still the safe haven it used to be. The dollar index has depreciated by more than 8% since the start of the year, and the yield on 10-year Treasury bonds has increased by 50 basis points in the week following ‘Liberation Day tariffs’. Downside growth risks and upside inflation risks have pushed investors to demand more compensation for taking duration risk (a bond portfolio's sensitivity to interest rate changes). There is also growing anxiety about the government's ability to manage debt in a slow-growth environment, and unease about lower foreign investors demand for US Treasury bonds.

The role of the dollar as reserve currency has also declined as sanctions imposed by the US and its allies on Russia following the invasion of Ukraine – freeze of half of its official foreign reserves, ban of selected Russian banks from the international payment system SWIFT – led Russia to diversify away from dollar into renminbi and gold.

Are there any alternatives?

A narrative is now emerging among investors that we are seeing the end of US exceptionalism. However, alternatives to the dollar often lack the depth, liquidity and other financial attributes required to appeal to global investors. In fact, while the eurozone financial markets are also large, they are fragmented across different countries and the euro does not have the same global reach as the dollar. As for the yuan, it still faces many challenges, including strict control over capital flows in China and a legal system that does not fully adhere to the principles of the Rule of Law. It would then require some major structural changes to dethrone the US dollar, and it would take time.

Over the short to medium term, uncertainty around trade policy will continue to weigh on the dollar. A decline in its role as a safe-haven currency could bring it closer to purchasing power parity, which is the rate of currency conversion that tries to equalise the purchasing power of different currencies by eliminating the differences in price levels between countries. According to this theory, a half-way correction in the fair value of one euro would be around 1.25 dollars, representing a further 10% depreciation of the dollar.

Increasing diversification

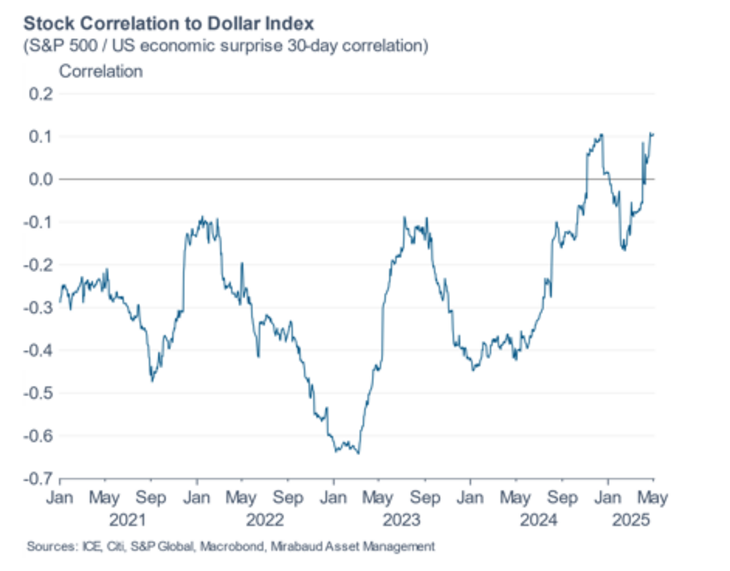

Whether or not this means the end of the dollar's international role, the current economic landscape has significant implications for asset allocation. The dollar has become increasingly correlated with equities, driven by rising stagflation risks and diminishing US exceptionalism. This correlation underscores the importance of traditional safe havens like gold and the Swiss Franc as crucial diversifiers in investment portfolios.

For equities, diverging inflation trends across countries are paving the way for potential policy divergence.

Europe may experience disinflation and more aggressive rate cuts from the European Central Bank, the Swiss National Bank and the Bank of England, while the US faces rising inflation and a more neutral monetary policy stance. As the world moves towards deglobalisation, business cycles are likely to become less synchronised.

This scenario highlights the importance of international equity diversification and exposure to alternative asset classes, such as hedge funds, to hedge against a potential recession in the U.S. The reallocation away from US assets has already begun, driven by a loss of confidence among international investors following the ‘Liberation Day tariffs.’

For decades, US bonds have served as a key buffer against recessions. However, their effectiveness has significantly diminished in the current environment. International diversification is expected to exert upward pressure on real yields, necessitating higher exposure to European bonds. This strategic shift in asset allocation aims to mitigate risks and capitalise on emerging opportunities in a rapidly evolving global economic landscape.

Información importante

La presente publicación ha sido elaborada por Mirabaud. No está destinada a ser distribuida, divulgada, publicada o utilizada en ninguna jurisdicción en la que dicha distribución, divulgación, publicación o uso esté prohibido. No está dirigida a personas o entidades a las que resulte ilegal enviar dicha publicación.

Leer más

Continuar con