“Content is King”. Why Media M&A is likely to accelerate

“Technology will liberate publishers to charge small amounts of money, in the hope of attracting wide audiences.” So said Bill Gates in his essay titled “Content is King”, way back in 1996. Technology is naturally deflationary, and with communication costs having tumbled, internet access speeds doubling every 18 months (over the last 40 years, “Edholm’s Law”), ease of access (App economy, smartphones, smart TVs) and consumers’ willingness to pay for entertainment – the opportunity of economic returns for differentiated content now far outweigh the threat of “cord cutting”.

There is a long history of Media M&A deals in the US; from AT&T/Time Warner, to Disney/21C Fox, to Comcast/Sky, to Discovery/Scripps and CBS/Viacom. Indeed, since 2014, there has been over $700bn spent in strategic M&A deals across the media and entertainment sectors (Reuters). Unprecedented change driven by technology has forced companies to consider transactions—such as merging with a fierce rival—that would have been unthinkable years before. Companies may also need to invest in adjacent offerings or shift out of their comfort zone, such as Disney’s aggressive pivot to DTC (Direct to Consumer). Disney’s strategic shift was years in the planning, culminating in the acquisition of 21st Century Fox. The Disney-Fox combination brought together Walt Disney Studios (including the previous acquisitions of Marvel, Lucasfilm and Pixar); Disney theme parks and hotels; ABC TV stations; A&E networks; Disney Channels; ESPN, Disney products and stores, music and publishing; Twentieth Century Fox studio; Fox’s TV production (“The Simpsons,” “Modern Family,” “This is Us”); cable networks FX, FXX, FXM and National Geographic channels; Star India; more than 350 international channels; controlling ownership of Hulu; and other assets. Their movie slate includes Avatar, new and earlier Star Wars films and unites Fox’s Marvel films — X-Men, Fantastic Four and Deadpool — with Disney’s Marvel properties. Then what happened next? Disney+. This streaming service launched in late 2019, set ambitious targets of creating over 100+ titles per year and aimed to reach 60-90 million subscribers five years after launch. With the success of original shows like “The Mandalorian” and Disney’s extensive library content, the service surpassed 100 million subscribers just 16 months after launch. Disney now expects to reach between 300-350 million subscribers by 2024.

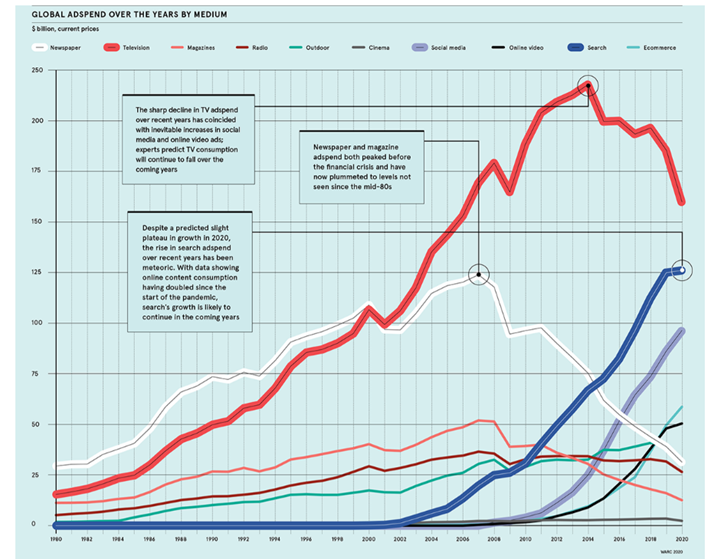

Just like in eGaming, which we follow very closely, the key to success in Media and Entertainment is CONTENT. This has been one of the key drivers behind megadeals as viewers increasingly seek original content and the rise in binge watching; both have been factors in Netflix’s rise from upstart to content and mind share leader. There is a general unwind of putting all content across all distribution platforms which had occurred in the early part of the last decade. In the early 2010s, content owners were willing to sign deals with the devil (aka the fierce rival that is Netflix) and give them distribution rights as any revenue was better than no revenue, and Netflix was considered to be too ‘alternative’ to become a threat to big media. But now Netflix is a direct competitor and content is the hook, with streaming the most disruptive use case in the industry.

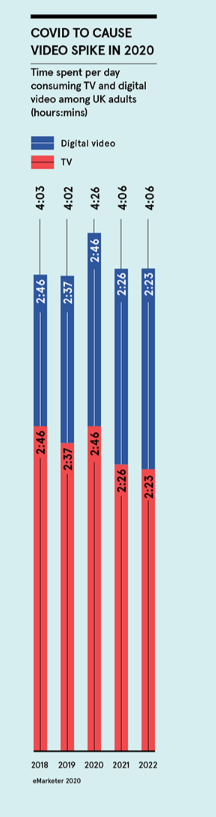

Reflecting the move to digital viewing, 80% of consumers use at least one streaming video service, up from 49% three years ago. Some broadcasters/producers moved earlier than others - Disney beat others in terms of timing, launching Disney+ and acquired Hulu via 21C Fox, and also by the surprise move of going for quick scale ahead of profit by using the weapon of low price. Others have struggled including Peacock (Comcast) or HBO Max (AT&T). In this uber-competitive streaming environment, one can opt for different strategies; from highly targeted content narrowcasting for specialised audiences to higher volume show counts with broad, popular appeal. However, there is a commonality regardless of type – namely the need for a reliable, easy to use platform and a sizeable programming inventory (Apple TV+ miniscule offering and More 4’s slow app and aggressive ad push are examples of what not to do).

Another way for platforms to differentiate themselves to brands and advertisers is by investing more in analytics and data technologies to offer more targeted ads and provide better insights on viewers (How did Netflix know you would like The Crown?!). This differentiator is built on targeted advertising, content customisation and recommendation engines, advanced data storage and analytics, and machine learning—plus the skill sets to support them.

Many advertisers are leveraging data-driven capabilities to differentiate themselves through technology, aiming to optimise efficiency with improved measurement, attribution, and analytics capabilities. These can enable advertisers to acquire audiences most likely to match and engage with certain products and strategies. Regardless of the targeting form, marketing partners’ overall objective is to achieve increased efficiency and effectiveness in moving consumers from awareness (advertising impression) to conversion (sales revenue) driving greater ROI from campaigns. This focus drove Comcast’s acquisition of advertising platform Freewheel. Having said this, capitalising and monetising data is both the hardest to execute and most likely to be an afterthought for many media companies. For companies traditionally focused on producing and distributing content, attaining depth in areas such as advanced analytics and advertising technology is furthest from their comfort zone—and more aggressive strategies such as directly acquiring these capabilities might be the most efficient solution.

It often comes back to content and, right now, there are too many offerings in the streaming market, and the path to ‘Mega Media’, from the result of consolidation, seems likely in our view. In May 2021 alone there has been a deal to merge Time Warner Media and Discovery to create a content behemoth, Amazon has spent $8.4B to acquire James Bond and the MGM Studios (and was reported to be interested in trying to buy Sony’s movie business) and France’s two leading commercial broadcasters M6 and TF1 have announced plans to merge to accelerate the development of a “French streaming champion”. We expect the pace of Media M&A to continue through 2021, and beyond.

Diese Veröffentlichung wurde von Mirabaud erstellt. Sie ist nicht zur Verteilung, Verbreitung, Veröffentlichung oder Nutzung in einer Gerichtsbarkeit bestimmt, in der eine solche Verteilung, Verbreitung, Veröffentlichung oder Nutzung untersagt wäre. Sie ist nicht für Personen oder Unternehmen bestimmt, an die die Übersendung dieser Veröffentlichung rechtswidrig wäre.

Mehr lesen

Weiter zu