In recent years, the Federal Reserve has faced increasing political pressure, particularly from former President Donald Trump. Trump publicly criticised Chair Jerome Powell for maintaining interest rates in the 4.25%–4.5% range, advocating instead for a sharp cut to around 1.0%. He accused Powell of costing the U.S. economy “a fortune” and even floated the idea of replacing him before the end of his term in 2026.

Such overt political interference poses a significant threat to the Fed’s credibility. Market participants closely monitor the central bank’s independence, which is essential for the effectiveness of monetary policy.

Recent declines in the U.S. dollar and the yield curve, as well as higher Fed rate cuts expectations reflect a broader reassessment of the central bank’s independence and its future policy direction.

Moreover, Trump’s suggestion to preemptively name Powell’s successor risks undermining Powell authority and disrupting the Fed’s carefully calibrated communication strategy, which relies on consistency, transparency, and a data-driven approach.

The Federal Reserve’s structure and its importance

The Fed institutional design is intentionally structured to resist short-term political pressures and safeguard long-term economic stability. Its governance model balances independence with accountability through three core components:

- The Board of Governors: Based in Washington, D.C., this federal agency comprises seven members appointed by the President and confirmed by the Senate. Governors serve staggered fourteen-year terms, and the Chair serves a renewable four-year term. This structure limits the influence of any single administration.

- Twelve Regional Reserve Banks: Located across the country, these banks represent diverse regional economic conditions, ensuring that monetary policy reflects the breadth of the U.S. economy.

- The Federal Open Market Committee (FOMC): The Fed’s main policy-making body, responsible for setting the federal funds rate. It includes all seven Governors, the New York Fed President, and four rotating Reserve Bank Presidents. This structure ensures a plurality of views and reduces the risk of centralized political capture.

How decisions are made?

The FOMC meets eight times a year to assess economic conditions and determine the stance of monetary policy. While decisions are made by consensus, they require formal votes by the twelve members. The Chair, currently Jerome Powell, plays a pivotal role in guiding discussions and communicating policy decisions to the public and financial markets.

Political pressure on Chair Powell and its implications

Chair Powell has resisted political pressure, emphasising the importance of understanding economic developments, particularly the effects of tariffs and inflation trends, before adjusting policy. His cautious approach prioritizes inflation control over short-term political demands.

Trump’s pressure and talk of early replacement have unsettled markets. The yield curve, which reflects interest rates across different maturities, is highly sensitive to Fed policy and credibility. Recent declines in 10-year and 2-year Treasury yields highlight market uncertainty about the Fed’s independence and future policy direction. Undermining the Chair’s credibility could weaken the effectiveness of monetary policy and increase market volatility.

Hawkish vs. Dovish tendencies among Fed voters

Hawks prioritise controlling inflation, favoring higher interest rates and tighter policy.

Doves emphasise supporting employment and economic growth, favoring lower rates and more accommodative policy.

Christopher Waller and Michelle Bowman, two members appointed by Trump, are currently among the more dovish members of the Federal Reserve and have expressed openness to cutting interest rates as soon as the July 2025 FOMC meeting.

Risks of naming Powell’s successor early

Trump’s suggestion to name Powell’s successor before the end of his term could disrupt the Fed’s communication strategy and compromise its independence. Early announcements risk politicising the role of Fed Chair, undermining Powell’s authority and eroding market trust in the Fed’s commitment to data-driven decision-making.

Powell has not indicated whether he plans to remain on the Board after his chairmanship ends in 2026. This uncertainty complicates Trump’s potential efforts to appoint a successor. Powell’s current term as Governor runs until 2028, meaning he could remain on the Board even after stepping down as Chair. This limits the administration’s ability to appoint a new Governor who could be elevated to Chair, making succession planning more complex.

Summary

The Federal Reserve operates through a carefully balanced governance system designed to insulate monetary policy from political interference. Chair Powell’s resistance to political pressure underscores the Fed’s commitment to its dual mandate of price stability and maximum employment. However, ongoing political pressure and speculation about succession risk unsettling markets and complicating the Fed’s ability to manage the economy effectively.

What lies ahead for monetary policy?

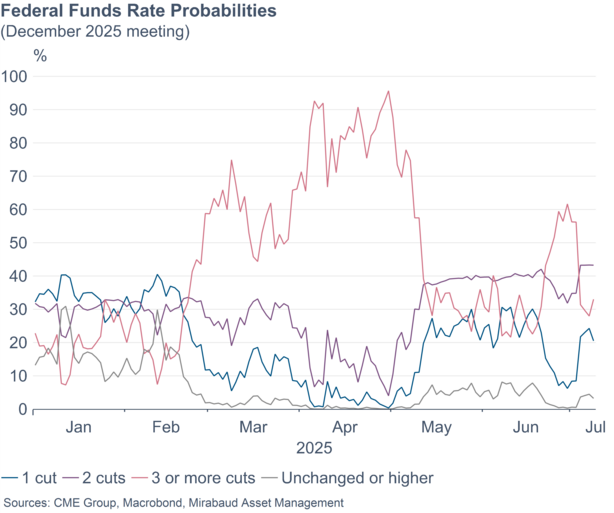

Market expectations for rate cuts have recently become more dovish, with a 35% probability of three cuts by year-end. These expectations are generally supportive of risk assets, assuming the U.S. avoids a recession.

Two key factors have shaped this outlook:

- Milder-than-expected inflation from tariffs: While tariffs initially raised inflation concerns, their actual impact on consumer prices has been less severe than anticipated, easing immediate inflationary pressures.

- Slowing economic growth: Signs of deceleration, including a slight contraction in Q1 2025 and concerns about labor market softening, have increased expectations that the Fed will cut rates to support the economy.

Chair Powell has noted that the Fed might have cut rates earlier if not for the inflationary effects of tariffs. However, with tariffs maintaining upward pressure on prices, the Fed remains cautious, balancing inflation risks against slowing growth. Overall, markets anticipate a gradual easing cycle once tariff-related inflation pressures subside, and economic conditions warrant further support. We expect two rate cuts this year, in September and December.

Información importante

La presente publicación ha sido elaborada por Mirabaud. No está destinada a ser distribuida, divulgada, publicada o utilizada en ninguna jurisdicción en la que dicha distribución, divulgación, publicación o uso esté prohibido. No está dirigida a personas o entidades a las que resulte ilegal enviar dicha publicación.

Leer más

Continuar con