With the recent sell-off, is SBC (Stock-Based Compensation) back in focus for technology companies?

There is a massive ‘gap’ between NON-GAAP and GAAP earnings. And this movie has been seen before – 20 years ago.

The 2002 Sarbanes Oxley Act was the start – it established rules regarding disclosures, governance, auditing reporting and risk management. The big thrust of this Act was in response to excessive managerial, equity-based compensation plans and there have been several studies to show that executive stock options and pay-risk sensitivity drove managerial responsiveness to risk-taking incentives. Then there was, in 2004, the Federal Accounting Standards Board who changed the standards and required that companies value stock options based on their fair value and record them as an expense on their grant date.

There are several studies of what is described as the pre-SOX period (that is pre-Sarbanes Oxley, and not the SOX Index) that finds a positive relation between managerial compensation incentives (primarily executive stock options) which incentivise managers to make riskier bets (Datta et al. 2001, Agrawal and Mandelker 1987, Coles et al. 2006).

Fast forward to 2022 and there are GAAP-earnings of course. So - it shows full disclosure of these incentives. Therefore, as the theory goes, the size or impact of these incentives don’t matter, because they aren’t hidden. But as shareholders, it does. Because GAAP earnings are ‘real’ numbers. The rather amusing definition of Non-GAAP is that GAAP doesn’t portray the true operations of a business so a company can disclose Non-GAAP (to display their own accounting figures) if they provide a reconciliation between adjusted and regular expenses. Now Non-GAAP often exclude one-off or non-cash expenses such as acquisitions, restructuring or one-time balance sheet adjustments - with the ideology that they show a clearer picture of the ‘real’ business and smooth out earnings volatility. But the non-cash expenses of Non-GAAP allows the inclusion of share issuance and the employee compensation through stock. The justification, of course, is that SBC (Stock-Based Compensation) is a reoccurring expense and so could be used in this non-GAAP calculation. On the other hand, as the saying goes; “Lies, damned lies, and Stock-based compensation”.

Investors may have turned a blind eye to this practice – ‘perhaps because all the tech companies do it’ or it isn’t perceived as an issue during a bull market when everything goes higher. But when this music stops… there are many implications. The glaring hole in real (GAAP) earnings for one. The excessive levels of stock comp for another. So, one might ask, does SBC (Stock-based compensation) matter? Perhaps Mr Warren Buffett puts it best, “If options aren’t a form of compensation, what are they? If compensation isn’t an expense, what is it? And, if expenses shouldn’t go into the calculation of earnings, where in the world should they go?”

Many companies reward employees with stock to attract and retain talent. Now, if they didn’t provide them with that stock, they would instead have to give them cash to attract and retain them, which would obviously have been expensed. Thinking about this the other way round – if some companies have been more aggressive about giving SBC than others – are they at greater risk of losing ‘talent’ when the stock price goes south? And if tech companies start losing their best execs and sales leaders – that would be a problem. Especially in 2022 - when talent pools have been drained, and there is rampant wage inflation everywhere because of a lack of available workers.

When one thinks of the high growth tech complex, particularly software, cloud, and SaaS providers – most investors value them on an EV/Sales basis. Why? Software is one of the few sectors that has been able to generate significant revenue growth during this last economic cycle of low growth. This scarcity, combined with the Fed’s aggressive monetary policy has driven higher valuation multiples – and drove software valuations to all-time highs, which contrasts with difficulties experienced in other sectors. Then if PE, VC and M&A view valuations are added in, the fixation on growth makes sense. Venture capital investors focus primarily on revenue multiples and future growth prospects, including market size and products/intellectual property, given that they are investing in immature companies. Private equity investors focus on revenue and EBITDA multiples, cost synergies and growth prospects, including the potential to leverage add-on acquisitions. A common theme for both PE and VCs is the importance of revenue metrics. So, while traditional financial metrics such as P/E and FCF Yields have been cast aside; revenue growth, P/Sales, EV/Sales, - growth, growth, growth… has become all that matters for many investors. This can then manifest itself in several other metrics.

ARR and monthly recurring revenue (MRR) are presently considered the most important metrics for software and SaaS companies. ARR and MRR are generally calculated by aggregating the total daily contracted revenue as of a specific point in time and either annualising it, in the case of ARR, or converting to monthly for MRR. MRR is used for companies that are oriented towards month-to-month or monthly invoiced contracts. ARR is often seen as an indicator of the predictability of revenues for a software company. Companies with higher ARR can be more precise in their revenue forecasts and to achieve those forecasts, which is attractive to investors. Since ARR annualises contracted revenues at a given point, it is also often interpreted as a real-time indicator of a company’s revenue growth as compared to GAAP revenues, which for SaaS or subscriptions can lag the actual contracted bookings. The predictability of ARR and subscription revenues yields much higher valuation multiples versus perceived one-time revenues from on-premise licenses or usage-based charges.

ARR is particularly important to PE investors as banks are often willing to lend more based on the predictability of revenues. If a PE firm can borrow 75% of the purchase price of a software company, they will likely be willing to pay a higher valuation than if they were only able to borrow 40% of the purchase price. Therefore, revenue predictability and robust ARR translates directly to higher exit valuations. Therefore, ARR has become such a fixation for investors in SaaS companies.

So ends the history lesson.

It is also serves as the explanation for the following exercise. With the fixation on revenue growth, and the acceptance during the bull market of stock expense (because it is seen as helping fuel the revenue growth), it is worth another look at which companies have been the most “generous” with SBC.

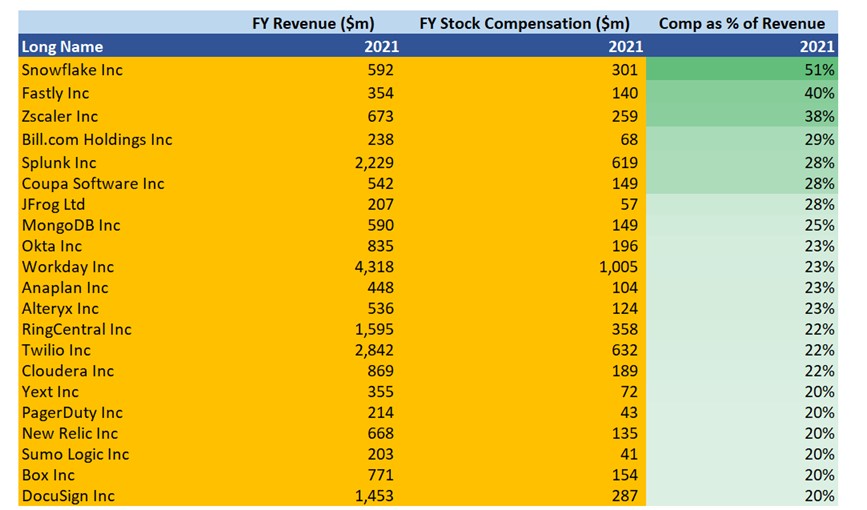

Some SBC schemes are overly generous. There have been examples of lock-up expiries being cancelled to allow for insider stock selling (just before a profit warning – Skillz at $30/share, last seen at $2). Or SBC quarterly value way above actual revenue values (Snowflake post IPO). But putting all that aside… and trying to simply present fact based on data – here is our findings of the very, very generous companies. And, a secondary consideration is, if employees’ stock strike price is severely underwater – which companies could be at risk of huge intellectual capital (people) turnover/loss? (This output is based on sectors/stocks/ETF constituents in the technology industry.)

We found 22 companies in the screen we ran which seemed to be very “generous” with their SBC plans. Namely they all paid out the equivalent of 20% of revenues or more in stock-based compensation in 2021. “Winner” of the most generous award went to Snowflake, followed by Fastly and Zscaler. See table below:

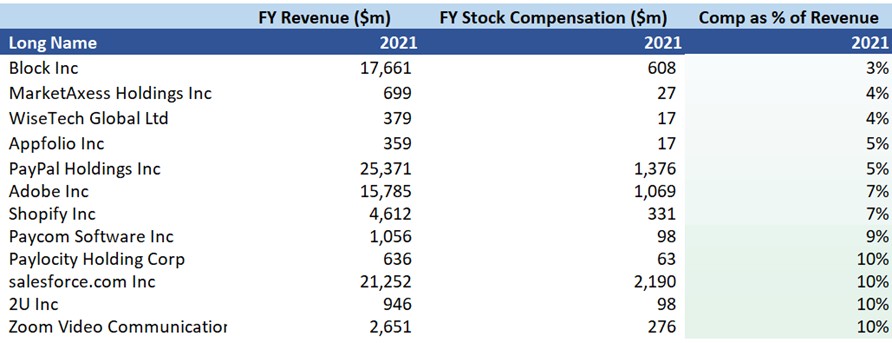

But in the same sector analysis there are some companies that seem much more shareholder friendly, in balancing their growth strategies, SBC levels and ratios. Among them are some well-established tech names such as Adobe, Salesforce and PayPal, and a couple which were surprising to see in this list because they are also some of the most aggressive growth companies (that tend to be found in the high comp v revenue ratio analysis above) such as Shopify and Block (Square).

If that stock comp, from an employee perspective, isn’t worth as much as it used to be, the best Tech job in the next year or two might not be in coding, nor in sales and marketing…but in Tech HR. Just when the Achievers Workforce Survey shows that 52% of FTE’s intend to look for a new job this year, up from 35% last year.

La presente publicación ha sido elaborada por Mirabaud. No está destinada a ser distribuida, divulgada, publicada o utilizada en ninguna jurisdicción en la que dicha distribución, divulgación, publicación o uso esté prohibido. No está dirigida a personas o entidades a las que resulte ilegal enviar dicha publicación.

Leer más