ESG Considerations, Real World Impact and Alpha Generation

There is certainly no shortage of “events” currently afflicting the world. The Q2 results season has confirmed that inflation of raw materials, transport and labour has arrived and is significant. Covid-19 uncertainly also persists, with a tug-of-war between vaccine rollout and the emergence of new strains muddying the waters over the pace of recovery. Meanwhile, US-China tensions continue to simmer on the backburner.

To that macroeconomic soup can be added a recent spate of extreme weather events, including severe drought in Brazil, fires in the US and devastating floods in China and Germany. The immediate impact of that has been to further stress already disrupted supply chains. Yet to our mind, the bigger picture is that such weather also serves to underline that whatever may be happening in the world, scratch the surface and the secular push around tackling climate change and energy transition is never far away. Indeed, even as Covid-19 presents an immediate challenge to the world’s policy makers, we note that the EU recently published a raft of proposals to reduce carbons emissions, stretching from bans on petrol and diesel vehicles through to loft insulation.

In recent months, we have also seen ESG considerations hamper a UK IPO (Deliveroo) and we note that the share price of Boohoo, which plunged last year on allegations of slave-like conditions in its supply chain, has yet to regain its past peaks. In short, ESG matters and the fact that ESG considerations are becoming ever more embedded in government, corporate and investor agendas suggests its relative importance is only set to further increase.

Nor is ESG a specialist area anymore. Our analysis, discussed below, reveals a compelling correlation between a company improving on ESG metrics and share price outperformance. At the same time, we also detect signs of increased pragmatism with respect to what sort of companies qualify as ESG friendly, with “Sinners to Saints” a clear theme for the year.

Defining an ESG investment strategy has always been something of a challenge and our favoured metaphor remains one of blind men standing around an elephant. On one level, an ESG investment strategy could simply mean the refusal to invest in certain sectors such as Tobacco or Defence; the lines blurring with an ethical investment strategy. For others, ESG credentials may effectively form a “license to invest”, with traditional investment returns still very much the objective (aided by ESG metrics underpinning quality). ESG can also be an end unto itself, this time the lines blurring with sustainable investing, as capital allocation is targeted towards companies developing new technologies for carbon capture, plastic recycling etc. To that can be added still more complexity over the relative importance of the environmental versus social and governance measures, let alone what, exactly, should be measured.

Market dynamics in the year-to-date also argue that a more pragmatic approach to defining ESG-friendly stocks is becoming more relevant. For a time, being classically “green” was itself enough for a company to enjoy a lot of love from the market. The likes of Orsted (windfarms), Nel (hydrogen) and Scatec (solar) all enjoyed rip-roaring share price outperformance into the end of 2020. Yet on our fundamental screening, such “chasing” of green stocks has also left many trading with extraordinarily high hope-for-future built into their valuations, often poorly supported by profit expectations on a normal investment timeframe (see examples below for Nel Hydrogen and Blink Charging).

In the year-to-date, many of those traditional “green” companies have endured significant share price wobbles. Yet at the same time, “dirty” companies like BP and Volkswagen, both in the process of transitioning towards greener business models, have outperformed. We see that as symptomatic of a broader “Sinners to Saints” theme and increased pragmatism towards defining ESG-friendly investments.

It also dovetails with our thoughts around “real world” impact. New hydrogen fuel cell technology may be sexy for those so inclined and indeed, such technology may well one day change the world. In the meantime though, the largest “real world” gains from an environmental and social standpoint will surely come from the transformation / transition of existing businesses.

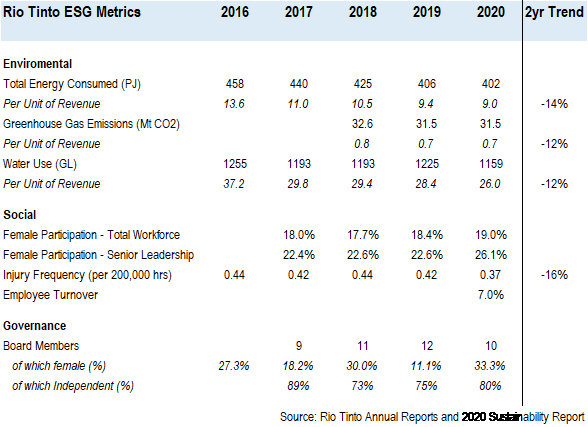

Mining company Rio Tinto is a case in point. There is certainly an argument that the act of digging resources out of the ground is an inherently unsustainable practice and for pure-play ESG funds, we fully accept that investment in mining companies is likely to be awkward / impossible. However, Rio Tinto’s existing scale means the group is also in a position to have a meaningful real world impact.

In the table below, we have picked out a number of KPIs to assess Rio Tinto’s momentum across the three broad areas of ESG. On the various environmental metrics, we find a broad based and substantial improvement. Total energy consumption has fallen 12% over the past four years on an absolute basis and from a per unit of revenue perspective, the improvement is 34%. Carbon emissions also seem to be on a sustained downward trajectory and the group’s water usage has fallen 30% over the past four years on a per unit of revenue basis.

On the social metrics, the overall proportion of female employees is fairly low but we suspect that is typical for the industry. Overall though, the proportion has trended higher over time. Rio Tinto’s female workforce also over-index in management positions. Also noteworthy is the single digit employee turnover percentage. With respect to Governance, Rio Tinto’s shareholders benefit from there being a high proportion of independent directors. Female participation at board level is also significant and has trended higher over time.

Overall, Rio Tinto may operate in a problematic sector but broad based improvement across many areas suggests the company is at the forefront of positive change. At a time when many traditional “green” stocks trade on punchy valuations, the transition of unloved environmental “Sinners” may well provide scope for higher investment returns plus a meaningful climate impact.

We have run similar ESG performance benchmarking for all the companies in the Stoxx Europe 600 index and have also benchmarked each company relative to its key peers. Through that exercise, we find clear evidence for a link between a company showing broad based improvement on its ESG metrics and share price outperformance.

On our analysis, the number of companies that have improvement in the three individual areas of ESG has definitely increased since we first ran the exercise back in 2019. On our latest screening, 53% of companies in the Stoxx Europe 600 Index show improvement on a three year view on around environmental standards, for example, compared to 49% in 2019. On social measures, 51% of stocks show improvement this year vs. just 35% in 2019 and on governance, 52% screen as having improved against just 32% in 2019. Such overarching trends would tend to support the view that ESG considerations are rising up the boardroom agenda, albeit plenty of companies have also deteriorated on a three year view.

We have also run a simple test to see what proportion of stocks in the Stoxx Europe 600 index have both improved on a three year view and whose share price has outperformed over January 2018 to July 2021 period. Improve in any area and there does seem to be some disposition towards outperformance, with ~55% of the companies that show improvement in any one area of ESG outperforming the index. The proportion rises to 57% for companies that screen as improving in at least two areas and that benchmark as outperforming peers. Improve in all three areas of ESG and benchmark as at least neutral against peers in three areas and the ratio rises to 78%.

Beyond ESG improvement being its own reward, we do see some fundamental explanations for that. There is an efficiency element to improving on the environmental measures, for example, potentially creating some cost advantage. On the social metrics, reduced employee turnover is likely to indicate a happier and more productive workforce. Good governance is also its own reward and resilience and adaptability through the Covid-19 crisis is likely to have been recognised by the market.

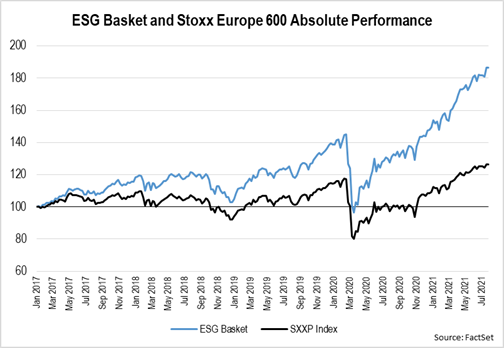

In the chart below, we have created an ESG basket from the Stoxx Europe 600 companies that show net improvement in at least two areas of ESG and that benchmark favourably against peers in at least two areas. The chart below assumes an investor had purchased an equal amount of each name on 1 January 2017.

On a relative basis, the basket has outperformed 48% over the time period, which for a mechanically selected basket based purely on their ESG credentials is remarkable. We do accept that this is a retrospective view but it is difficult to ignore the correlation between ESG improvement and share price outperformance. The implication is a simple one: the relevance of ESG considerations now goes far beyond the ESG specialist and we certainly see a case for consideration of ESG factors to be widely built into the investment process.

La presente publicación ha sido elaborada por Mirabaud. No está destinada a ser distribuida, divulgada, publicada o utilizada en ninguna jurisdicción en la que dicha distribución, divulgación, publicación o uso esté prohibido. No está dirigida a personas o entidades a las que resulte ilegal enviar dicha publicación.

Leer más

Continuar con