Weekly Thoughts by Mirabaud Securities - 26 July 2019

All eyes on the European Central Bank (ECB) this week, before the Fed next week. Equities rose once again on hope before Mario Draghi disappointed. The ECB president said he told the Group of Seven, meeting earlier in July, that “it’s difficult to be gloomy today” because there are signs of strength, even if there is quick deterioration in other areas…. Indeed, the S&P 500 and the Nasdaq hit new highs on Wednesday. In Europe, the week was supportive for the DAX and the OMX. The Italian MIB and the SMI on the other hand lost more than 1%. The MSCI World Equity Index, which tracks shares in 47 countries, gained almost 1% on the hope of central banks intervention. In Asia, MSCI’s broadest index of Asia-Pacific shares outside Japan rose 0.3%.

Although, the escalating tensions between the EU and Switzerland over the Swiss equities trading ban cooled off the franc appetite, the euro-swissy broke this week the 1.10 mark, far below the Swiss National Bank’s (SNB) ideal 1.20 handle. Pricing on the three-month Euro-Swiss franc futures, on the other hand, suggests that the market is convinced that a further SNB policy action could be needed, especially if the European Central Bank attempts to lower its rates by the end of this year. The dollar was strong against all the G10 currency members. In emerging markets (still vs. dollars) most of the currencies were weak. The biggest loosers of the past week were the Colombian peso, the Brazilian real and the Chilean peso. The only winner was the Chinese yuan.

The automotive sector has never been so depressed in Europe. These include geopolitical ructions such as US trade disputes with Europe and China, as well as the Brexit. The implications of the Worldwide Harmonised Light Vehicle Test Procedure (WLTP) laboratory test, used to measure fuel consumption and CO2 emissions from passenger cars as well as their pollutant emissions, do not help either. The question is now: did we touch the bottom? There are several reasons to believe that a tactical rebound could occur in a recovery stage driven by cost reduction, decrease in the effects of the WLTP cycle, new tax reductions in China for the second quarter, the possibility that the worst of the global auto production is behind us, valuation being supportive and an ECB dovish tone (supports cyclical stocks). In the future, investors face challenging decisions when selecting winners of the future automotive industry. Yet, there are compelling common themes that will underlie all successes in an electrified industry. The most obvious is the development of battery technology which, itself, is reliant on sourcing key commodities such as cobalt, lithium and manganese. Like the gold rushes of olden times, it may be the battery equivalent providers of picks and spades for gold diggers who end up being the real winners in the electrification of the automotive industry.

According to Bloomberg calculations made from the quarterly data of Eurostat, France has squeaked past Italy to become the country with the biggest debt load in the euro area in absolute terms. Its debt-to-GDP ratio is still just below 100%, compared with Italy’s 134%, and the nation’s borrowing costs are far, far lower, but the dubious honor may undermine its moral high ground when it comes to lecturing Italy’s government about its controversial budget plans. In a report, France’s Cour des Comptes said the growing divergence between France and its neighbours on debt reduction was “worrying” and “could lead to a deterioration of the perceived quality of France’s debt among investors”. It chided the government over its failure to take advantage of a spell of growth to significantly rein in overspending, which leads to increased borrowing every year. “France is far from having eliminated its structural deficit whereas many of its European neighbours have achieved a balance,” it warned in a 150-page report. No French government has balanced the books since the 1970s. Will further negative interest rates help the country to softer the pressure on its debt charge?

What will stop the luxury sector? Difficult to answer if you look at LVMH results this week as the luxury firm capitalised on strong Chinese demand and investments in marketing & new designs. The industry’s top players are riding high on demand for branded goods across Asia and particularly in mainland China, in spite of a Beijing-Washington trade war that could ultimately weigh on consumer sentiment. Within Paris-based LVMH, the world’s biggest luxury conglomerate, Louis Vuitton is betting on temporary pop-up stores to spike consumer interest and has turned to DJ-turned-designer Virgil Abloh to grow its menswear lines. Its Christian Dior brand, while still estimated to be less than a third of Louis Vuitton’s size, was also one of the standouts of the second quarter, with sales growth exceeding the 20% of the broader fashion and leather goods unit. Overall, LVMH, whose other labels include champagne maker Moët & Chandon, said second-quarter sales across the group rose 15% to 12.5 billion euros ($13.9 billion) euros, up 12% at stable exchange rates and a comparable number of stores.

Several hot topics were discussed this week, including:

The American growth is not dead / The ECB studies revamping inflation goals/ Opportunistic purchase on the auto sector / Is French debt sustainable? / The ECB meeting

Please feel free to ask for more information if interested.

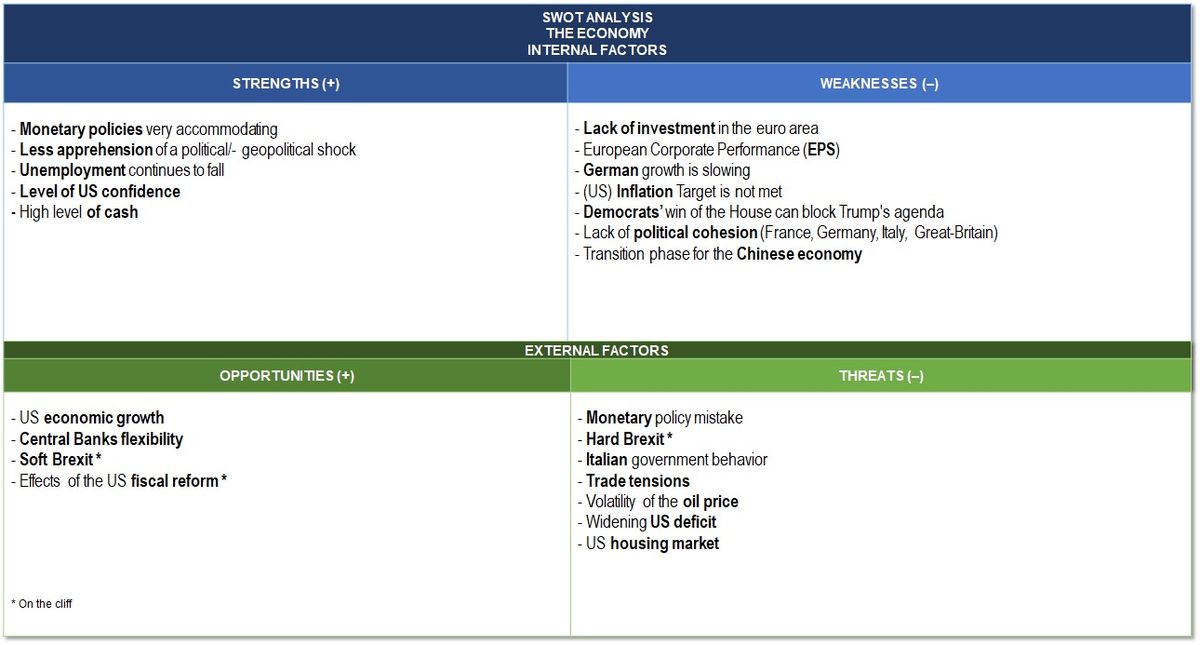

“Effect of the US fiscal reform” (Opportunities) as we expect a fading fiscal stimulus in the coming months.

SWOT stands for Strengths, Weaknesses, Opportunities and Threats, the French equivalent of FFOM analysis (Forces, Faiblesses, Opportunités et Menaces). While SWOT analysis can be used to develop a company's marketing strategy and evaluate the success of a project (by studying data sets such as company's strengths and weaknesses, but also competition or potential markets), I decided several years ago to adapt it as a way to analyse financial markets. SWOT analysis allows a general development of markets by crossing two types of data: internal and external. The internal information taken into account will be the strengths and weaknesses of the market. The external data will focus on threats and opportunities in the vicinity. Finally, and most interestingly, there is a table that will evolve according to current events, which will allow it to reflect the underlying trend in the financial markets on a weekly basis.

This publication is prepared by Mirabaud. It is not intended to be distributed, disseminated, published or used in any jurisdiction where such distribution, dissemination, publication or use would be prohibited. It is not intended for people or entities to whom it would be illegal to send such publication.

Read more

Author

Continue to