Weekly Thoughts by Mirabaud Securities - 29 March 2019

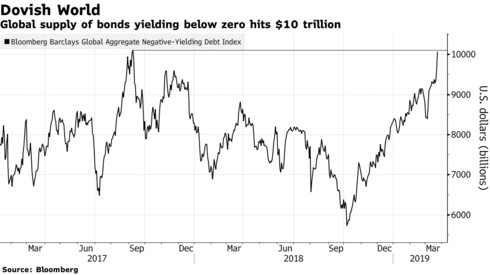

Yields on T-Bonds, which contract 10 points below the Fed's interest rate, the German Bund, which falls below the Japanese 10-year level for the first time since 2016, or the inversion of the US 3-month/10-year yield curve; this week was marked by significant movements in rates that will certainly be remembered for a long time. However, the indices continued to rise with the S&P 500 progressing by almost 0.5% (on Thursday evening). The same movement occurred for the Euro Stoxx 600 over a week, fuelled by the ECB President's comments about the impact of negative rates on banks. In Asia, the Nikkei fell sharply (-2.5%) as a result of worry about the impact that a global economic slowdown could occur. The sanctions topic were even more important for Chinese indices as the Shanghai Composite lost -3.5% and once again goes against the consensus.

The Swiss Franc was the main focus of this week, sending a strong signal when it fell below 1.12 against the Euro. This is all the more surprising given that several negative reports have emerged concerning Switzerland, whether in a survey concerning a resurgence of pessimism within the financial community on the future of the Swiss economy or the Swiss KOF Institute Spring Economic Forecast cut (GDP growth of 1% for 2019, against 1.6% expected until now).

There is now a significant gap between what the currencies and the indices tell us (in fact the same gap as between the indices and the rates). If some are accusing the Swiss National Bank (SNB), it is unlikely they are the cause. Indeed, it is difficult to see how the national institution could avoid supporting "its currency" when all the indicators are red for exporters.

An attack against the Swiss currency is also unlikely, as several funds have already broken their teeth in the past. Rather, we see a renewed interest from "foreign" investors trying to hedge against indices that have gone (according to them) too high too fast and before crucial deadlines such as Brexit or the trade negotiations between Washington and Beijing.

In recent years, streaming services such as Netflix, Amazon Prime and Hulu have swiftly evolved to become one of America's favorite ways to consume video content. These days, there are more digital media and entertainment options offered than ever before and a new survey from Deloitte shows just how much progress streaming has made.

U.S. households now subscribe to three paid streaming services on average and, notably for the first time, more households subscribe to a video streaming service than traditional pay television. In fact, 69% of households have at least one streaming video subscription, compared with 65% who have a cable subscription.

Despite the acceleration of cord-cutting, the survey also revealed that some consumers continue to pay for streaming and cable TV, with 43% of consumers having subscriptions to both. Deloitte's 2018 survey found that streaming video adoption breached the halfway mark in 2017 with 55% of consumers subscribing to streaming services.

The trend is evident; cord-cutting is expected to explode this year through 2021. Traditional TV is now in deep trouble and could be heading to its death?

Once again, the good student of the week is Portugal. Portugal's budget deficit fell sharply to 0.5 percent of gross domestic product last year, compared to 3 percent in 2017, reaching its lowest level since 1974. The National Statistics Institute (INE) said the deficit was 913 million euros in 2018, compared to 5.77 billion euros in 2017 (hit by the "extraordinary recapitalisation operation" of 3.94 billion euros for state-owned Caixa Geral de Depósitos bank), the year when economic growth reached its highest since the turn of the century. Finance Minister Mário Centeno had already estimated the 2018 deficit to be around 0.6 percent of GDP, 0.1 percent lower than the 0.7 pct initially forecast by the government. The 2019 deficit might fall to 0.2 percent of GDP. The only problem is that public debt as a percentage of GDP is still very high (121.5% in 2018) but has fallen compared to 2017 (124.8%).

Apple had a difficult week this week.

First, announcing a suite of new services Monday, Apple said it struck agreements to bring its enhanced TV app -- with access to a la carte network subscriptions and, eventually, Apple's original content -- to smart TV devices from rivals like Samsung Electronics Co., Amazon.com Inc., and Roku Inc.

Apple also said it would provide a physical credit card, so people who sign up for its new Apple Card payment service can make purchases at locations that don't accept Apple Pay. Such deals are a departure from a formula that has been at the center of Apple's success since the original Macintosh; selling gadgets and software that were inextricably linked -- you couldn't buy one without the other.

That approach, which gives Apple control over users' experience, has proven enormously profitable. Apple cleared nearly $60 billion in profit last fiscal year on $266 billion in revenue; about two-thirds of sales came from the iPhone.

Second, a U.S. trade judge recommended Qualcomm Inc to win on a patent dispute. ITC administrative law judge MaryJoan McNamara said the basis for the ban was a finding that Apple infringed on a Qualcomm patent relating to smartphone technology.

Several hot topics were discussed this week, including:

Who will be responsible for tomorrow's growth? / Is television dead? / The Fed is about to launch a Twist operation / What if Obamacare disappeared? / The online dating business

Please feel free to ask for more information if interested.

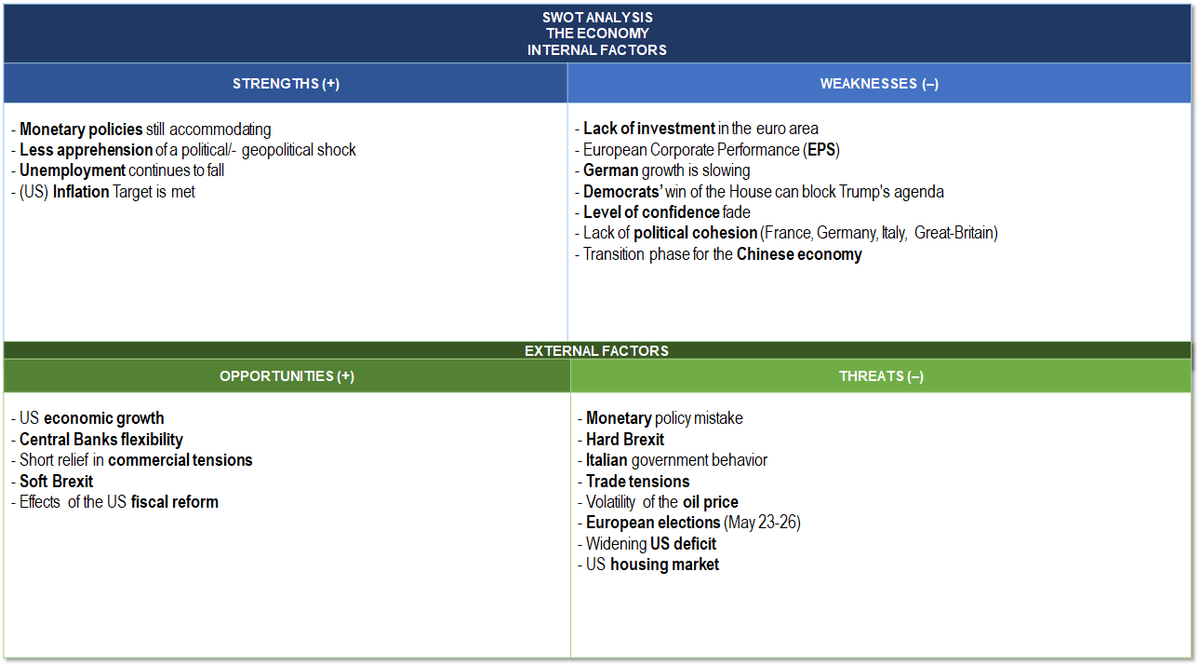

“(US) Level of confidence fade” (WEAKNESSES) is on the cliff this week. Consumer confidence surged in February and rose for the first time in four months, a sign that Americans have regained optimism after the recovery in the U.S. stock market, the end of the government shutdown and diminished worries about recession.

SWOT stands for Strengths, Weaknesses, Opportunities and Threats, the French equivalent of FFOM analysis (Forces, Faiblesses, Opportunités et Menaces). While SWOT analysis can be used to develop a company's marketing strategy and evaluate the success of a project (by studying data sets such as company's strengths and weaknesses, but also competition or potential markets), I decided several years ago to adapt it as a way to analyse financial markets. SWOT analysis allows a general development of markets by crossing two types of data: internal and external. The internal information taken into account will be the strengths and weaknesses of the market. The external data will focus on threats and opportunities in the vicinity. Finally, and most interestingly, there is a table that will evolve according to current events, which will allow it to reflect the underlying trend in the financial markets on a weekly basis.

This publication is prepared by Mirabaud. It is not intended to be distributed, disseminated, published or used in any jurisdiction where such distribution, dissemination, publication or use would be prohibited. It is not intended for people or entities to whom it would be illegal to send such publication.

Read more

Author

Continue to