Weekly Thoughts by Mirabaud Securities

The week (to Friday) was marked by a profit taking from the American indices after the dovish ECB meeting. The S&P 500 couldn’t hold the 2800 points support level. This breach could indicate a full test of the 2640 level. The market is at risk of seeing a very leveraged strategy turning to a net seller. The question now is whether we are experiencing a consolidation before a new bounce or whether there is a profit taking of several percent (10%?) taking place. In Europe, while the EuroStoxx50 was down by only 0.2 percent (in local currency) this week, we noticed that the SMI suffered from the sharp rise in the Swiss Franc, which penalized export stocks. Finally, in Asia, Chinese indices finally dropped (-0.7% for Shanghai composite for example) despite largest credit injection ever...

In the G10 environment (against the dollar), it is the Scandinavian currencies that suffered the most this week, with the Norwegian Krona ahead of the Swedish krona and the Danish krona. The Japanese Yen was the only winner against the dollar. In emerging markets (against the dollar) the Argentine Peso, the Brazilian Real and the South African Rand and the Turkish Lira suffered the most this week. On the other hand, the Indian rupee was the only currency to rebound against the dollar. Finally, investors sold the Euro to US Dollar (amid concerns about the Eurozone slowing growth outlook and the dovish ECB meeting).

LVMH, Gucci or Moncler: Chinese shoppers might have lost their appetite for iPhones, but they are still buying luxury. Luxury companies LVMH, L'Oreal and Hermes have also defied expectations of weaker sales in China caused by a slowdown in the world's second largest economy. Several elements could fuel the rise in the sector's values in 2019: e-Commerce, Chinese youth, US millennials, the development of marketing on social networks and a consolidation of "physical stores". While there are obviously risks (geopolitical, currency fluctuations, slower growth or commercial risks), it will be necessary to be extremely selective by betting on shoes, jewellery and bags. However, the "mid-range" watch sector could still suffer in the coming months.

The central bank unexpectedly re-assessed its forward guidance and as a result announced a fresh round of 2-year TLTROs (TLTRO-3) starting in September. In the same line, the ECB stands ready to use all available tools in order to lift inflation expectations. At his press conference, President Draghi noted the near-term outlook for economic growth appears weaker than anticipated, while the ECB now sees the economy expanding 1.1% in 2019 (from 1.7%), 1.6% in 2020 (from 1.7%) and 1.5% in 2021 (unchanged from previous forecasts). Regarding inflation, the ECB expects consumer prices to rise 1.2% this year (from 1.6%), 1.5% next year (from 1.7%) and 1.6% in 2021 (from 1.8%). As a reminder, price stability (ECB mandate) is defined as a year-on-year increase in the Harmonised Index of Consumer Prices (HICP) for the Euro area of below 2%. The next rate hikes might appear soon…

Wall Street analysts are increasingly bearish on Deutsche Bank, with 31 of the 32 analysts covering the company not suggesting to buy the stock. In fact, 18 say "sell," 13 say "hold," and just one says "buy." The lone analyst recommending the stock (Bankhaus Lampe), does not have a single "sell" rating on any of the 14 companies in his coverage universe. The German bank is dealing with a number of issues including a $1.6 billion loss on a municipal bond trade, increased funding costs, and a host of legal challenges. The company has paid more than $18 billion in legal fines over the past decade, an amount on par with its current market capitalization of $18.9 billion. In the wake of dealing with a number of scandals many employees' bonuses are being cut severely and some bankers in New York and London will get zero pay-outs.

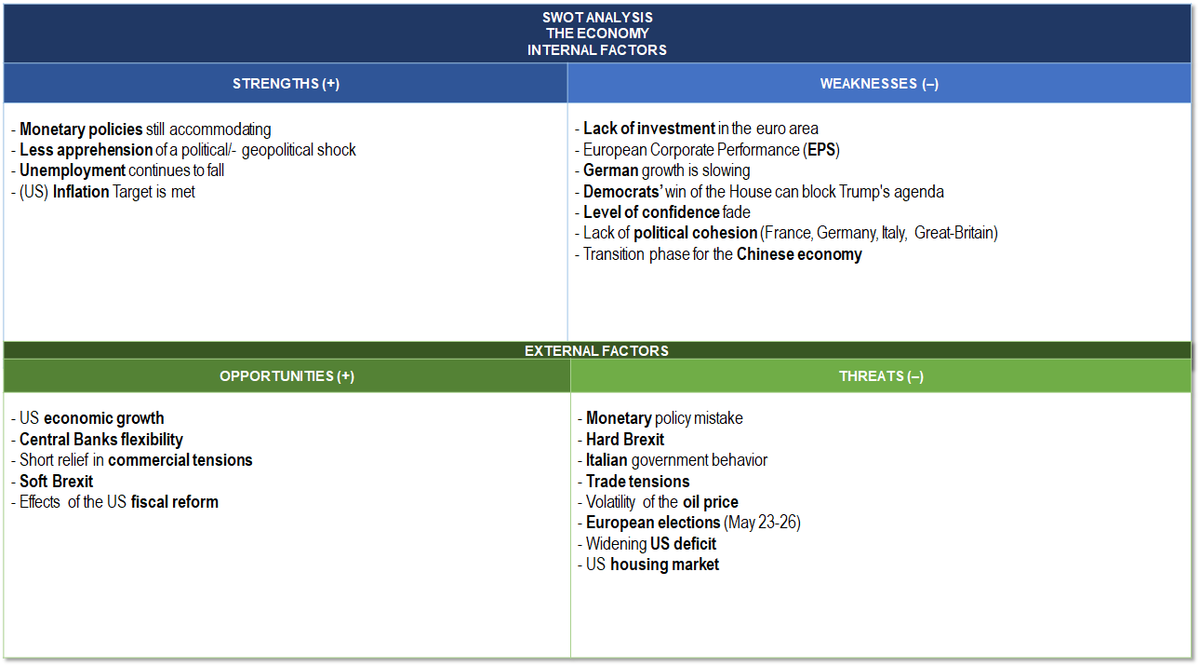

Several hot topics were discussed this week, including: February Report / Luxury sector: time to buy? / Investing in Gen Z / Beige book / ECB Meeting

Please feel free to ask for more information if interested

This publication is prepared by Mirabaud. It is not intended to be distributed, disseminated, published or used in any jurisdiction where such distribution, dissemination, publication or use would be prohibited. It is not intended for people or entities to whom it would be illegal to send such publication.

Read more

Continue to