Weekly Thoughts by Mirabaud Securities - 20 December 2019

After Boris Johnson's broad victory in the British parliamentary elections and Sino-American promises to have a trade agreement in early January 2020, the indices were, as expected, in pause mode and some investors took their profits this week. Over the week, the main American indices ended with no real trend. The same boring trend for European indices with an average increase of nearly 0.25%. In Asia, most of the indices were fueled by hope trade talks between Washington and Beijing will resume shortly.

Turkish lira is the biggest looser of the week (against the dollar) after the U.S. Senate passed legislation with provisions to punish Ankara, raising concerns about already strained ties with Washington. The lira has lost more than 11% this year after a currency crisis chopped its value by 30% last year. Ties with the United States have been troubled by policy differences in Syria and Turkey’s purchase of Russian S-400 missile defence systems, which prompted Washington to move towards imposing sanctions. Still at the emerging market level most of the members' currencies (against the dollar) experienced increases over the week with a significant overperformance for Chilean peso and the South Korean won. At the G10 level, the Norwegian krona was the best performer, followed by the Canadian dollar. The Australian dollar and the British pound finished the week negatively against the dollar.

Few people know it, but in Switzerland, until recently, a mobile phone was called NATEL (for Nationales Auto-TELefonnetz), a word invented in 1975 with the introduction of the first Natel A in 1978, followed by the Natel B in 1980, a 12 kg mobile bag. Nearly 40 years later, Apple's market cap is well over a trillion dollars, thanks to the iPhone’s success. The same is true for companies such as Huawei or Xiaomi. However, the trend is evolving radically. The market may soon begin to pale next to the sums commanded by the sale of products and services that depend on smartphone ownership—the so-called “smartphone multiplier.” From selfie sticks and ringtones to mobile ads and apps, smartphone multiplier revenues may eclipse the revenue generated by smartphones themselves in just a few short years. Deloitte predicts that the smartphone multiplier will drive US$459 billion revenue in 2020 alone. This represents a 15 percent (US$58 billion) increase over the prior year, already greater than the US$26.6 billion (6 percent) year-over-year growth that smartphones may see in 2020. With smartphone sales in 2020 expected to reach US$484 billion, the entire smartphone ecosystem—smartphones plus smartphone multipliers—will be worth over US$900 billion.

Demographic dynamism, sustained growth, digital evolution, the emergence of a strong entrepreneurial and innovative spirit has made the Indian market a particularly attractive investment compared to other emerging economies. In addition, more than 65% of the population is under 35 years of age and large segments of the country is well educated and speak English. Finally, India has attracted a number of foreign investments, notably from Japan and the United States. However, 2020 could be the year of disappointment for this country of nearly 1.4 billion people. One after the other, rating agencies, major banks and the World Bank have reduced India's growth forecasts, where GDP should not increase by more than 6% this year (fiscal year April 2019 to March 2020. The problem seems to be deeper than it seems, especially since India's economic output growth slowed to 4.5% (from 5% in the previous quarter) in the three months ending in September, its lowest level since the first quarter of 2013. The country's weightings are fourfold: slower investment, low consumption, financial stress for rural households and a decline in job creation. The Indian authorities have taken the bull by the horns by relying on two crucial aspects: massive stimulus and rate cuts. To summarize, India is now at a major turning point for its economy. Indeed, China's growth relay is struggling and will even fall below Chinese growth this year. While the Indian authorities (political and monetary) have already announced important measures, the question is whether they will be sufficient to prevent the country from growing below 4%.

After an annus horribilis for Boeing following 2 fatal accidents that killed 346 people, the American company announced the indefinite suspension of the 737 MAX production starting beginning of next month, due to the delay in certification. Priority will be given to the delivery of the 400 single planes assembled since March, with no redundancies or technical unemployment expected "for the time being". The financial consequences of this shutdown of the Renton FAL, the first since 2008, will be detailed at the end of January when the fourth quarter results are presented; according to some analysts, the suspension of deliveries of 737 MAX since last March would cost it USD 4.4 billion per quarter. The latest estimates published show also that the inventory situation could cost up to one third of US GDP growth in the first quarter of 2020...

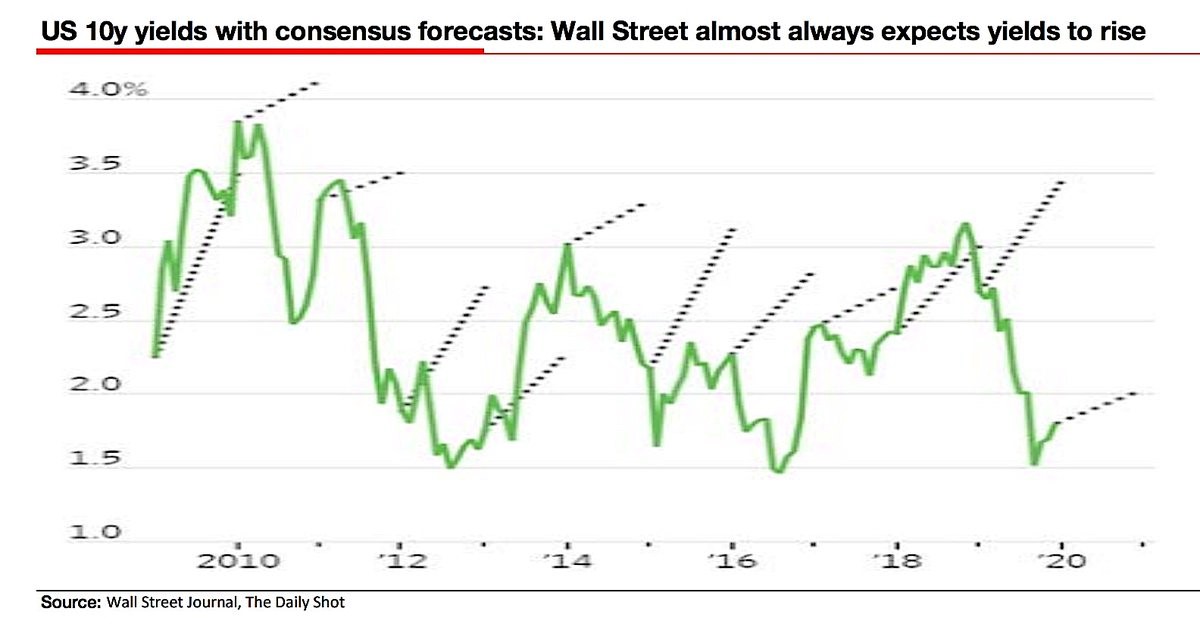

Several hot topics were discussed this week, including:

Smartphones are dead, long live the smartphones / India misses the relay / Sweden goes into positive rates / Liquidity, nothing else / Portugal: first in class

Please feel free to ask for more information if interested.

* On the cliff

SWOT stands for Strengths, Weaknesses, Opportunities and Threats, the French equivalent of FFOM analysis (Forces, Faiblesses, Opportunités et Menaces). While SWOT analysis can be used to develop a company's marketing strategy and evaluate the success of a project (by studying data sets such as company's strengths and weaknesses, but also competition or potential markets), I decided several years ago to adapt it as a way to analyse financial markets. SWOT analysis allows a general development of markets by crossing two types of data: internal and external. The internal information taken into account will be the strengths and weaknesses of the market. The external data will focus on threats and opportunities in the vicinity. Finally, and most interestingly, there is a table that will evolve according to current events, which will allow it to reflect the underlying trend in the financial markets on a weekly basis.

This publication is prepared by Mirabaud. It is not intended to be distributed, disseminated, published or used in any jurisdiction where such distribution, dissemination, publication or use would be prohibited. It is not intended for people or entities to whom it would be illegal to send such publication.

Read more

Author

Continue to