Weekly Thoughts by Mirabaud Securities - 22 November 2019

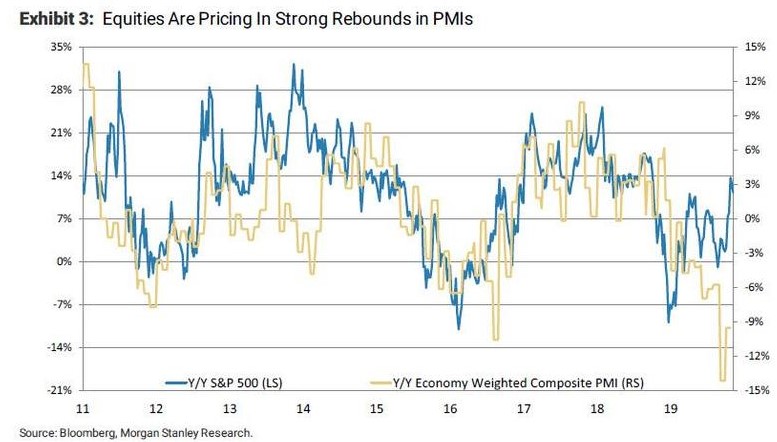

This week was a copy paste of the last one. Indeed, while there is still some doubt about the progress of negotiations between Washington and Beijing, the main American indices have reached new historic highs this week. The market seems overbought and still leads us to believe that a (healthy) consolidation should materialize soon. Over the week, the main American indices ended a bit lower. It’s the same small negative trend for European indices with an average decrease of nearly 1% despite the fact that the German economy avoids recession. In Asia, most of the indices were under the pressure of the Hong Kong turmoil and ended lower by nearly 1%.

New Zealand’s central bank left recently interest rates unchanged -- defying widespread expectations of a cut -- saying there are signs the domestic economy will stop slowing and that inflation will pick up. The New Zealand dollar jumped three quarters of a U.S. cent after the announcement. The RBNZ is betting that the easing it has delivered this year, including a surprise 50-point cut in August, will revive economic growth in 2020, helping inflation return to the midpoint of its 1%-3% target. Still at the G10 level, excluding the Canadian dollar, the swiss franc and the Japanese yen, all the members finished the week positively against the dollar (the New Zealand dollar was the best performer). At the emerging market level most of the members' currencies (against the dollar) experienced increases over the week with a significant overperformance for the Argentinian peso. The South Korean won and the Mexican peso managed to finish in red as well as the Philippine peso..

Wall Street’s exuberance over legal weed has quickly curdled into sober reality. In a matter of months, white-hot cannabis companies have flamed out in spectacular fashion. Many have lost two thirds or more of their value. Widespread legalization has been thwarted. Bank financing has dried up. Deep-pocketed institutional investors remain on the sidelines and old-fashioned black-market dealers still provide stiff competition. The pain deepened on Thursday, when Ontario-based Canopy Growth Corp. announced revenue that fell short of the lowest Wall Street estimate and a loss that one analyst called “astounding.” That sent shares to the lowest since December 2017. It’s still the largest pot company in the world, but at C$7.1 billion its market value is just a sliver of the C$24 billion it reached in April. One day later, MedMen Enterprises Inc., one of the first U.S. cannabis companies to sell shares to the public, said it would dismiss 190 employees, including about 20% of its corporate workforce, as it struggles to preserve a dwindling cash pile. Time to talk about a bubble burst?

As the trade war between the United States and China drags on, U.S. companies are weighing other options to avoid the tariffs currently levied on Chinese imports. In the first nine months of 2019, U.S. goods imports from Vietnam, Taiwan and South Korea surged 35, 21 and 7 percent, respectively, compared to the same period of last year, while imports from China dropped by 13 percent year-over-year. Vietnam in particular has been profiting from the trade dispute as it supplies many of the goods that U.S. companies typically sourced from China before the trade war. According to data from the United States International Trade Commission, cited by the Financial Times, U.S. imports of mobile phones from Vietnam more than doubled in the first four months of 2019 compared to the same period of last year, while computer imports rose by 79 percent. Footwear, textiles and furniture from Vietnam also saw a boost in demand from the U.S., as did fish, which was typically processed in China for consumption in the United States before the tariffs were introduced. The steep increase in U.S. imports from Vietnam has seen the Southeast Asian economy leapfrog several countries to become the seventh-largest import partner for the United States in the first nine months of 2019.

Some analysts think Home Depot is a leading indicator for the economy. Let’s hope not… The company said on Tuesday the marriage of its online and brick-and-mortar businesses was not yet generating as much revenue as it had expected, prompting the retailer to cut its 2019 sales forecast for the second time this year. Shares of the largest U.S. home improvement chain, which have risen nearly 40% this year, fell more than 5% on Tuesday, the worst in almost 10 years. To keep customers away from smaller rival Lowe’s Cos Inc (LOW.N), Home Depot invested heavily in its online business, primarily by adding automated lockers in stores for shoppers who want to pick up their orders rather than wait for them to be delivered. The company had previously cut its full-year sales forecast in August due to falling lumber prices as well as the anticipated impact new U.S. tariffs on Chinese imports would have on consumer demand. Home Depot’s weak results also pulled shares of the whole sector.

Several hot topics were discussed this week, including:

Long live consumption / Santa Rally? / Cannabis under pressure / Fed Minutes / RSI under the scope / Vietnam in pole position

Please feel free to ask for more information if interested.

* On the cliff

SWOT stands for Strengths, Weaknesses, Opportunities and Threats, the French equivalent of FFOM analysis (Forces, Faiblesses, Opportunités et Menaces). While SWOT analysis can be used to develop a company's marketing strategy and evaluate the success of a project (by studying data sets such as company's strengths and weaknesses, but also competition or potential markets), I decided several years ago to adapt it as a way to analyse financial markets. SWOT analysis allows a general development of markets by crossing two types of data: internal and external. The internal information taken into account will be the strengths and weaknesses of the market. The external data will focus on threats and opportunities in the vicinity. Finally, and most interestingly, there is a table that will evolve according to current events, which will allow it to reflect the underlying trend in the financial markets on a weekly basis.

This publication is prepared by Mirabaud. It is not intended to be distributed, disseminated, published or used in any jurisdiction where such distribution, dissemination, publication or use would be prohibited. It is not intended for people or entities to whom it would be illegal to send such publication.

Read more

Author

Continue to