Weekly Thoughts by Mirabaud Securities - 26 April 2019

When you are “running on empty,” it requires a lot of “hope” that you can make it to the next gas, or charging station before the engine quits running. The same is true with the markets. The current advance is unfortunately not built on improving economic or fundamental data but on hope. Hope that the economy will improve in the second half of the year, hope that earnings will improve in the second half of the year, hope that oil prices will trade higher even as supply remains elevated, hope the Fed will not raise interest rates this year, hope that global Central Banks will still be supportive, hope that the US Dollar doesn’t rise “too much”, hope that China will keep stimulating, hope that a “trade deal” will be concluded soon and hope that high-yield credit markets remain stable. Last Tuesday the S&P 500 ended the day just below its intraday record of 2,940.91. The Nasdaq closed up 1.3% at 8,120.82. The Dow Jones Industrial Average, meanwhile, gained 145.34 points to close at 26,656.39 and was 1.1% from an all-time high. In Europe the OMX was the champion of the week gaining more than 3%. The FTSE MIB lost almost 1% after the release of its budget for 2019 and 2020. In the emerging market, China (Shanghai) lost more than 5% and is now 33% away from its record high (2007). Japan gained almost 1% on the week, thanks to the Bank of Japan...

In the G10 universe (in dollars), it is the Swedish Krona that has suffered the most this week with the Australian Dollar and the Norwegian Krona. The Japanese Yen was the only gainer. It is interesting to note that the Euro is now at the lowest level against the dollar for approximately the past two years 2 years. In emerging markets (still in dollars), the Argentine Peso lost more than 8%, ahead of the South-African Rand and the Turkish Lira. The only (small) gainers were the Malaysian Ringgit (+0.13%) and the Hong-Kong Dollar (+0.03%).

The US pharma sector is actually facing several headwinds: drug pricing pressure from regulators, patients, politicians and payers, patent expiry of biologics, US Political divided, the “Amazon” effect and more recently the ambitious public health insurance plan backed by Sen. Bernie Sanders and several other Democratic presidential candidates as a solution to soaring U.S. medical costs. Most of the health care players, including Anthem, Cigna and HCA Healthcare, seemed to catch a cold. The market value of insurers and hospitals sank a total of $28 billion on Tuesday, noting that the swoon amounted to the worst five-day period for the health insurance industry in eight years. More broadly, health care is the stock market's worst-performing sector this year. But enough is enough. The US pharma sector seems now oversold (IHF US vs SPX lowest since 2017- and 14-week RSI lowest since the financial crisis). Though we are not fundamentally Bullish on the pharma sector, technically it’s a short time good buying opportunity.

The Bank of Japan, as expected, forecasted this week that inflation will remain below its 2 percent target through the fiscal year that ends in March 2022. In quarterly projections, the central bank slightly cut its growth and price forecasts for the current fiscal year, ending in March 2020, due to headwinds from slowing overseas growth. For the first time, the BOJ also released forecasts for fiscal 2021 that project inflation to move above 1.5 percent but fall short of 2 percent. With its 2 percent inflation target seen out of reach, the BOJ will join other major central banks that are being forced to delay plans to end crisis-mode policies due to soft inflation and growing signs of a global economic slowdown. Years of heavy money printing have failed to fire up inflation to 2 percent and left it with little ammunition to fight the next recession. Shinzo Abe’s economic plan (Abenomics) has clearly failed to bring the growth he promised, and more disappointment lies ahead with a slump in global demand and Japan’s continually ageing society. Hopefully the Nikkei is not reflecting the economic meltdown and is (almost) only depending on a low Yen and monetary stimulus. As a reminder, the Bank of Japan Is now a Top-10 shareholder in 50% of all Japanese companies...

A massive penalty hangs over Facebook’s head (the company recorded an accrual of $3.0 billion in connection with the inquiry of the FTC into their platform and user data practices), but it otherwise had a very strong Q1 earnings report. Facebook reached 2.38 billion monthly users, up 2.5 percent from 2.32 billion in Q4 2018 when it grew 2.2 percent, and it now has 1.56 billion daily active users, up 2.63 percent from 1.52 billion last quarter when it grew 2 percent. Facebook pulled in $15.08 in revenue, up 26 percent year-over-year. Facebook now has over 2.7 billion total mothly users across its family of Facebook, Messenger, Instagram, and WhatsApp, the same as last quarter. 2.1 billion people use at least one of those apps daily, up from 2 billion last quarter. Wall Street seems to have already priced in the potential FTC fine (that could cost between $3 to$5 billion dollars). Facebook has agreed to strict oversight of how it handled user privacy in a 2011 deal with the FTC. It promised to not misrepresent its privacy practices or change privacy controls without user permission, and it’s now negotiating the fine for potentially breaking those terms. As a reminder, Facebook has $45.2 billion in cash and securities on hand to pay a potential fine and make any necessary acquisitions.

Several hot topics were discussed this 2 last weeks, including:

Trump superstar / QE4, a good idea? / Italy - Greece: The unlikely match / Bond market: Beware of consensus / Beige book / Luxury and Pharmaceuticals Sectors: Two different destinies / Japan from every angle / The weight of excess in the S&P 500 / The dollar begins to impact

Please feel free to ask for more information if interested.

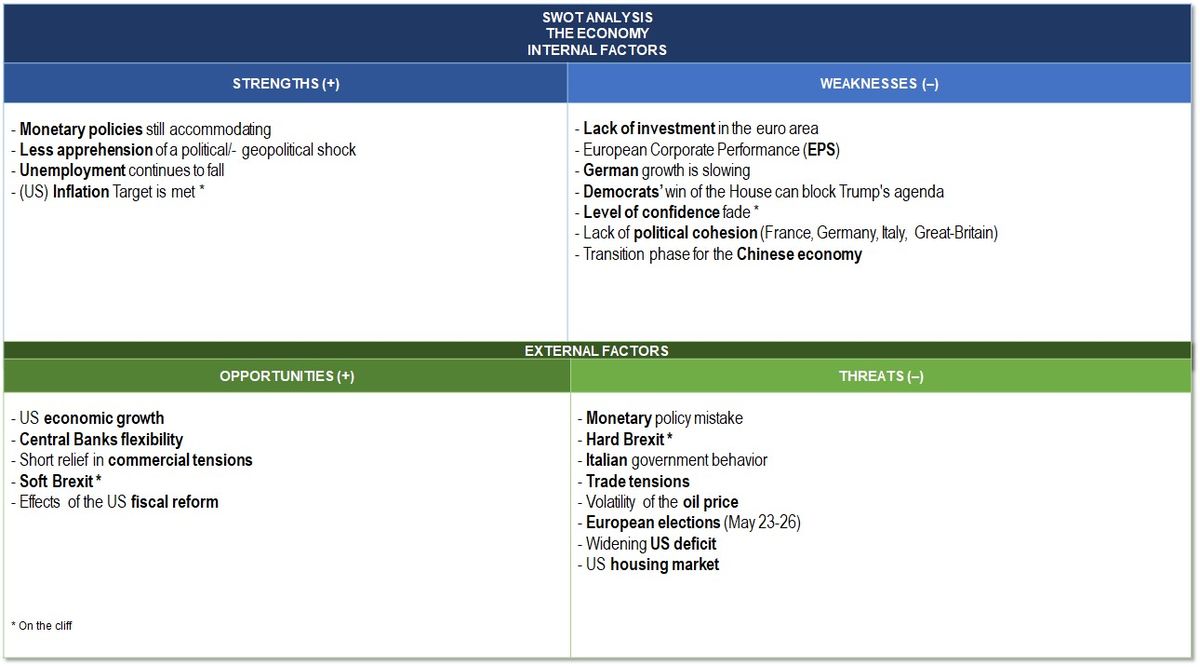

“(US) Level of confidence fade” (WEAKNESSES). Consumer confidence surged in February and rose for the first time in four months, a sign that Americans have regained optimism after the recovery in the U.S. stock market, the end of the government shutdown and diminished worries about recession.

“Hard and Soft Brexit” (Opportunities & Threats) is on the cliff this week after the Brexit was postponed to 31 October. There is still a risk, however, that the House of Commons will approve the withdrawal agreement before May 22nd.

SWOT stands for Strengths, Weaknesses, Opportunities and Threats, the French equivalent of FFOM analysis (Forces, Faiblesses, Opportunités et Menaces). While SWOT analysis can be used to develop a company's marketing strategy and evaluate the success of a project (by studying data sets such as company's strengths and weaknesses, but also competition or potential markets), I decided several years ago to adapt it as a way to analyse financial markets. SWOT analysis allows a general development of markets by crossing two types of data: internal and external. The internal information taken into account will be the strengths and weaknesses of the market. The external data will focus on threats and opportunities in the vicinity. Finally, and most interestingly, there is a table that will evolve according to current events, which will allow it to reflect the underlying trend in the financial markets on a weekly basis.

This publication is prepared by Mirabaud. It is not intended to be distributed, disseminated, published or used in any jurisdiction where such distribution, dissemination, publication or use would be prohibited. It is not intended for people or entities to whom it would be illegal to send such publication.

Read more

Author

Continue to