When Apple catches ‘a cold’, their supply chain gets the ‘flu’

Much has been made in recent years of Apple’s diversification in product lines, to take some pressure off the iPhone sales numbers. Apple has branched out to offer more service based products – Apple news, Apple Fitness, Apple music, Apple Arcade, iCloud, Apple TV, and so on. Despite these valiant efforts, the company still finds itself in a position where it is incredibly reliant on one product… the iPhone. In 2020, 50% of Apple’s Net Sales came through the iPhone (iPad 9%, Mac 10%, wearables, home and accessories 11%, and services 20%). Mind you, that sounds like a good ‘problem’ to have when you consider that Apple managed a single quarter, mid-pandemic, of $111B of sales (December 2020). For fiscal year just completed, Apple is expected to generate $114B of cash flow from operations. In other words, Apple is ‘printing’ $13 million of cash …. Every single hour.

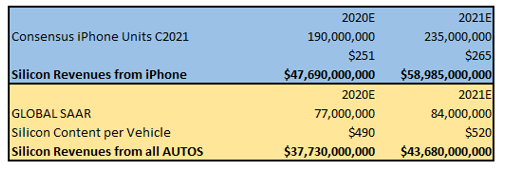

Back in 2009, the App Store passed the milestone of serving 2 billion apps. It fed the app economy, the app developers signing up, and helped drive iPhone sales. Today, there are over 1 billion active iPhones. And Apple reached 2 billion iPhone sales earlier this year. The iPhone is a big deal – not just for Apple, but also its supply chain. Apple is the largest purchaser and consumer of silicon chips in the world. In fact, on our calculations the single product category of the Apple iPhone alone generates more revenues for the semiconductor industry than the entire auto industry. The iPhone is likely to need $59B of semiconductors in 2021, compared to $44B for all auto OEMs combined.

Much has been made of the limited supply of semiconductors this year. It is the result of a plethora of factors; logistics issues, geographic fragmentation of the supply chain, under investment in back-end capabilities creating bottlenecks, utilisation yield issues (from substrate shortages to power cuts create problems – a fab forced offline can take a month to ramp back up) and a post-COVID recovery of demand. And capacity is a significant issue when you consider it can take two to three years to build a fabrication plant. So when supplies are limited and customers are put on allocation, the one company that is likely to get preferential treatment is the world’s largest buyer, Apple. But even Apple doesn’t escape the phenomena with news reports (breaking first from Bloomberg) that Apple is cutting production of iPhones by 10-15% for the key holiday quarter because it can’t source components.

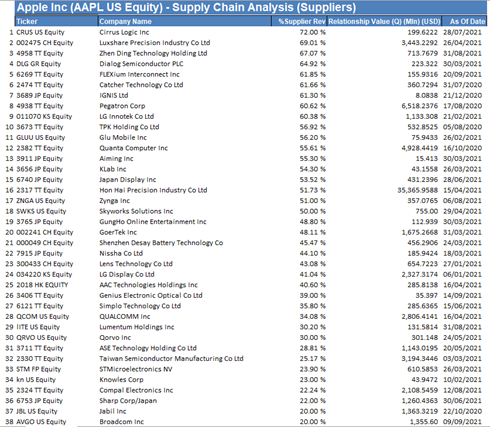

Apple suppliers could be negatively impacted by two interconnected forces at play, we feel; namely inflationary pressures on costs (higher Bill of Materials, BOM) and lower volumes. The big focus of the iPhone 13 this year for many is that there’s no price increase versus the 2020 models. This seems somewhat odd given that we know there are huge price increases in the silicon economy; from wafers (TSM’s most recent price increase on leading edge – aka Apple – was 10%) all the way through package and test. Then add in the logistics issues, raw material cost increases and wage inflation the world over. So what gives? What probably doesn’t give, too much, is those sacred device margins that the iPhone has enjoyed for the last 12 years in defying the economic cycles of all products which went before it. But someone, somewhere must be ‘wearing’ the impact – because we know that the consumer isn’t either. If you are an unavoidable TINA (there is no alternative) supplier to Apple, then you maintain pricing power (Taiwan Semiconductor as the sole manufacturer of the A15 chip, for example). But if there are multiple vendors for a solution, then they might be getting a call from the procurement head at Apple with a message that goes something like; “I know prices are up 20%, but I’m only paying +%. Take it, or leave it and I’ll go to your rival”. What would you do? While the iPhone is the cornerstone of Apple, it is also a key source of revenue for many of the OEM’s that produce its components. There are 38 companies, for example, who have 20% of revenues coming from Apple. IPhone sales are absolutely critical to their success too. The 2020 iPhone 12 blended BOM (Bill of Materials) came in 20% higher than the 2019 model average. Part of this won’t be repeated because of the shift from LCD to OLED, which led to part of the cost increase. But there were also higher costs from RF subsystems, 5G modem, and 5nm wafer costs. Given what has been happening this year; from wafer costs, commodity price increases (copper), logistic cost increases, wage inflation, back end assembly and test shortages and PCB price rises, something has to give.

The Apple ‘economy’ and their power is unmatched, and suppliers know it. They might face a cold winter.

Cette publication est préparée par Mirabaud. Elle n’a pas vocation être à distribuée, diffusée, publiée ou utilisée dans une juridiction où une telle distribution, diffusion, publication ou utilisation serait interdite. Elle ne s’adresse pas aux personnes ou entités auxquelles il serait illégal d’adresser une telle publication.

Lire plus

Continuer vers