Why Japan is our star pick for 2022

As we enter 2022, one thing is more apparent than ever; it is a Macro Market. Whether it be Growth/Value dynamics, China property implosion, Fed meetings or Commodity & Energy resilience; macro is currently in the driving seat. The increasing mechanisation of trading (factor baskets, ETFs) that has taken place over the lifetime of many Mirabaud brokers is partly responsible for this trend. The result: understanding the various political and economic forces is essential if you are to consistently make money. Stock picks out of context are dangerous as we enter the final stages of this long-term debt cycle…

Global Thematic & Strategy Team at your service.

Japan is our star pick for 2022. A potent combination of government stimulus, logical COVID strategy and industrial names set to blossom in the pivot away from China has caught our eye. All the while, Japanese stocks trade at rock-bottom multiples (trailing 12M P/E’s: Nikkei 16x, FTSE 300 21x S&P 26x) that don’t reflect the favourable low-inflationary environment they are operating within.

Tying this all together is the real possibility of more ESG-friendly funds moving into Japanese equities. As a key driver of actively managed flows, ESG poses a huge opportunity. Japan is just in front of Canada and Australia/New Zealand in terms of total ESG assets. However, Japan’s economy is almost 3x as large as these names. Should Europe, the current high-water mark for ESG saturation, become a new standard, then Japan could experience a 40-fold increase in ESG-driven asset allocation.

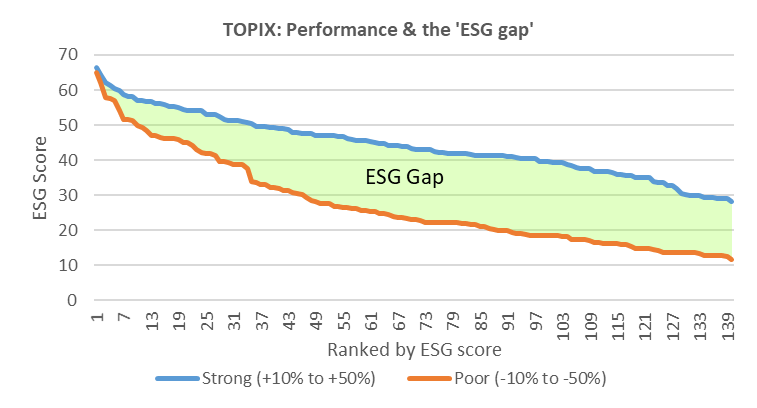

Taking out the TOPIX strong performers (+10 to +50%) and Poor performers (-10 to -50%) over the past year and ranking them by ESG score, we can see how the ESG profile of the two groups differs. This is the ‘ESG Gap’ in the Japanese market.

Japan has, and continues to, place significantly fewer impositions on the average citizen compared to other major economies (see chart below). This fills us with confidence that the Japanese government will handle Omicron sensibly and pragmatically, as it has done for previous COVID waves.

The Japanese government overcame a slow start in the vaccination race to achieve one of the highest rates of full vaccination globally; 79% as of Jan 12. Vaccines are only part of the story. Other factors have protected Japan throughout the pandemic. Firstly, it ranks #1 globally for hospital beds per head of population. Secondly, the Japanese population likely had some pre-existing COVID immunity: early immunology studies in 2020 revealed that a SARS-like coronavirus had circulated in the region before. This has helped to significantly push down the death rate, not just in Japan, but in much of China and Southeast Asia. Thirdly, a reliance on antiviral therapies has allowed the economy to stay on a relatively even keel. Japanese GDP shrank -4.6% in 2020 compared to the UK’s -9.8% drop.

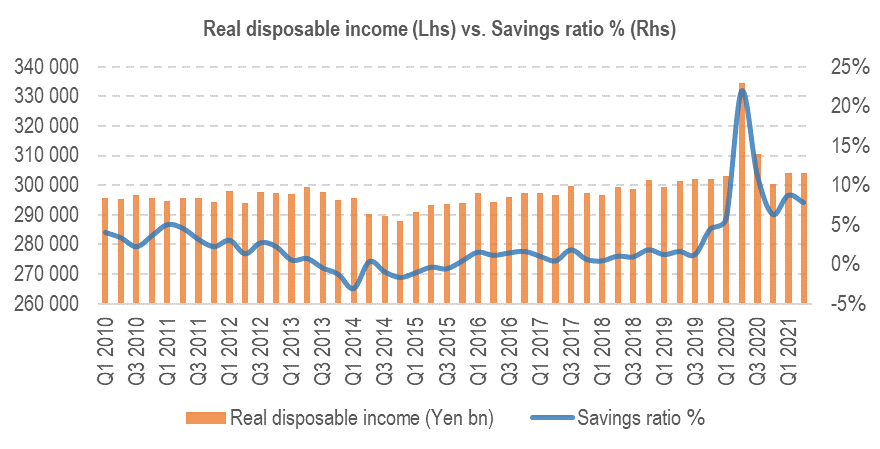

Governments and central banks the world over have been unwinding stimulus measures as economies run hot. The interest rate rise from the Bank of England (0.1% to 0.25%) and the hastened ‘tapering’ schedule from the US Federal Reserve in Q4 2021 were key signals that the tide is set to turn in 2022. Japan has, thus far, remained immune. In November, the newly minted prime minister - Fumio Kishida - announced a huge cash injection of $383bn USD. This programme, which is likely to conclude in the first quarter of 2022, includes a direct cash payment of ¥100,000 ($872) to low-income families with children under 18. The Japanese government has also been running a tourism campaign “Go To Japan” which covers 50% of travel costs up to ¥20,000 per night. This is set to be reinstated in February after pausing in November due to Omicron concerns. These are two headline policies that sit within a wide array of support packages for both individuals and businesses. The economy will be bolstered by this support through to Q3 2022. Heading into this period of stimulus support, Japanese savings rates were already strong and disposable income plentiful, as shown below.

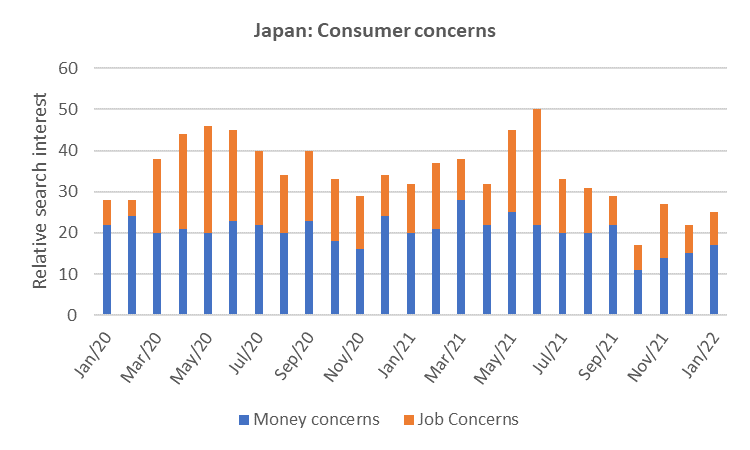

Importantly, this is filtering through into positive consumer sentiment. Real-time data shows that ‘jobless concerns’ and ‘cash concerns’ are low, chart below.

The Japanese government can continue to support the consumer in this way as inflation fears are almost non-existent. Current inflation is running at 0.1%. Haruhiko Kuroda, governor of the Bank of Japan, forecasts that inflation will increase to ~1% by mid-2022. Compare this to the 7.0% January CPI print in the US.

In a ‘Macro Market’, the minutiae of single stock coverage becomes less relevant. Scrutinising the detail, you might find yourself scratching your head as blue-chip investments backfire. It is vital to know which way the wind is blowing before setting foot into the market. In 2022, we believe it is blowing East, towards Japan.

Cette publication est préparée par Mirabaud. Elle n’a pas vocation être à distribuée, diffusée, publiée ou utilisée dans une juridiction où une telle distribution, diffusion, publication ou utilisation serait interdite. Elle ne s’adresse pas aux personnes ou entités auxquelles il serait illégal d’adresser une telle publication.

Lire plus

Continuer vers

Asset Management

Asset Management