Weekly Thoughts by Mirabaud Securities - 06 September 2019

New government in Italy, US-China trade breakthrough or Hong Kong extradition bill withdrawal, there were lots of arguments for the market to go higher. Over the week, the main American indices ended up sharply. The same positive trend for European indices with an average increase of nearly 1.5% despite talks about the Brexit outcome. In Asia, most of the indices were fueled by hope that the Hong Kong turmoil will end and that trade talks between Washington and Beijing will resume shortly.

The pound rebounded from its lowest level in 34 years (excluding a brief "flash crash" in 2016 that may have been caused by technical glitches during a highly volatile day of trading) as MPs attempted to block a no-deal Brexit and Prime Minister Boris Johnson lost his majority. At the G10 level, excluding the Japanese yen, all the members finished the week positively against the dollar (the Swedish krona was the best performer). At the emerging market level most of the members' currencies (against the dollar) experienced increases over the week with a significant over-performance for the Argentinian peso. Still in emerging markets, there were also notable increases in the Colombian peso and the Russian rubble. Only the Indian Rupee and the Chilean peso krone managed to finish in red.

A zombie company describes a firm that cannot meet its debt obligations without taking out even more debt or liquidating assets. That said, the longer interest rates stay low, the more the zombie population will multiply. In fact, across 14 advanced economies, zombies now number 12% of all publicly listed companies, according to a research paper by the BIS (Bank for International Settlements). Within the S&P 1500, 14% of companies could be classified as zombies, according to the BIS. In the 1980s, the share was a mere 2%. But in an era of rising rates , or a recession that pummels everybody across the board, there can be rude awakenings for companies that previously "looked" okay. It i’s not just the U.S. dealing with this problem, either. Since low rates are a global phenomenon, there are plenty of the Walking Dead lurching around in Europe and China, as well. One result of a global zombie economy is that productivity suffers.

It’s a big surprise that nobody is talking about: Australia’s economy grew at its slowest pace in a decade last quarter. Yet, GDP rose just 1.4% in the June quarter from a year earlier, data showed on Wednesday, matching the worst of the global financial crisis. If there was a bright spot in last Wednesday's numbers it was that quarterly growth of 0.5% matched market forecasts, when there had been fears it would be even weaker. Yet almost all the growth came from government spending and exports, with domestic consumption hamstrung by miserly wage gains and a sharp downturn in home building. In all, public spending added 1.3 percentage points to GDP growth in the year to June, with net exports another 1.2 percentage points. Household consumption, usually a powerhouse of the economy, added a tepid 0.8 percentage points to growth for the entire year, while spending on autos actually sank 7%. While households were struggling, Australia’s huge mining sector enjoyed a massive profit windfall from high commodity prices and strong Chinese demand. The Reserve Bank of Australia (RBA) has called for fiscal action, as it cut interest rates in both June and July to reach an historic low of 1%. Investors already believe a quarter-point cut by November is a done deal, with another pencilled in by March.

Shares in Aston Martin tumbled again and again this month as pressure continued to mount on the British luxury carmaker amid a broader market rout. The carmaker, based in Garydon, Warwickshire, last month downgraded its sales forecasts for 2019 from about 7,250 vehicles to 6,400, citing macroeconomic uncertainty in the UK and Europe, which face slowing growth and the threat of a no-deal Brexit at the end of October. Aston Martin’s weaker sales in the first half of the year – at a time when it needs to fund a new factory to build a make-or-break SUV, the DBX – have led many investors to question whether it will need to raise more money, potentially diluting the value of shares. The worsening outlook has added to financial pressures. Moody’s rating agency downgraded its rating on Aston Martin’s debt in July, making it more expensive for the carmaker to borrow money. Hedge funds have also taken out a record level of short bets that its debt will fall in value. Luxury carmaker is now worth now a fraction (5.46) of its £19 a share October 2018 listing price. As a reminder, Ferrari is trading near its record high…

Several hot topics were discussed this week, including:

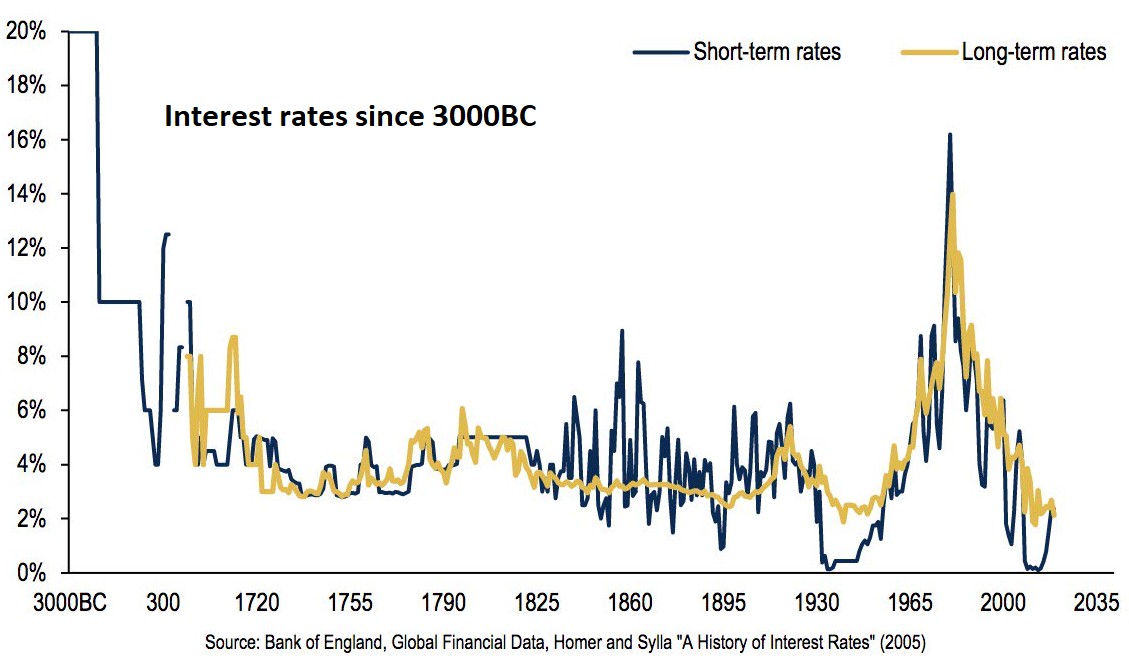

August review / American yields are too… high / Is value dead (again) / Walking Dead / The Jeremy Corbyn put

Please feel free to ask for more information if interested.

“Effect of the US fiscal reform” (Opportunities) as we expect a fading fiscal stimulus in the coming months.

SWOT stands for Strengths, Weaknesses, Opportunities and Threats, the French equivalent of FFOM analysis (Forces, Faiblesses, Opportunités et Menaces). While SWOT analysis can be used to develop a company's marketing strategy and evaluate the success of a project (by studying data sets such as company's strengths and weaknesses, but also competition or potential markets), I decided several years ago to adapt it as a way to analyse financial markets. SWOT analysis allows a general development of markets by crossing two types of data: internal and external. The internal information taken into account will be the strengths and weaknesses of the market. The external data will focus on threats and opportunities in the vicinity. Finally, and most interestingly, there is a table that will evolve according to current events, which will allow it to reflect the underlying trend in the financial markets on a weekly basis.

Diese Veröffentlichung wurde von Mirabaud erstellt. Sie ist nicht zur Verteilung, Verbreitung, Veröffentlichung oder Nutzung in einer Gerichtsbarkeit bestimmt, in der eine solche Verteilung, Verbreitung, Veröffentlichung oder Nutzung untersagt wäre. Sie ist nicht für Personen oder Unternehmen bestimmt, an die die Übersendung dieser Veröffentlichung rechtswidrig wäre.

Mehr lesen

Author

Weiter zu